Sustainable Finance

Sustainability Engagement with Customers

The SCSB projects to closely engage with clients by following the “Regulations for Sustainable Development Engagement” and designing the “SCSB Sustainability-linked Credit Extension Guidelines” to promote sustainable credit business. Moreover, the SCSB serves itself as the benchmarking management bank, and clients who achieve ESG indicators such as GHG emissions intensity, water consumption per unit of revenue, water consumption per unit of production, electricity consumption per unit of production, wastewater emission intensity, and suppliers' social responsibility, would benefit from rate cuts in return. This way, clients’ adherence to ethical management, environmental protection goals, and the fulfillment of achieving the sustainable finance management policy would be more effective consequently. At the end of 2024, the SCSB had processed 56 Sustainability-linked loans, with a total credit balance of NT$ 18.517 billion. Apart from internal guidelines, the SCSB aims to further promote ESG-centric consulting services in 2024 and assist SMEs in achieving low-carbon innovation developments, offering infrastructure-centric project loans for both managed factories and specific ones. At the end of 2024, the SCSB assisted in the completion of 1,325 applications, with a total lending balance amounting to NT$ 6.222 billion.

To reinforce sustainable engagement with individual customers, the SCSB has asked its Relationship Managers in personal finance to incorporate information related to financial services addressing environmental or social issues into the mortgage and loan application forms for personal finance starting from September 2023. At the end of 2024, the SCSB proceeded 6,285 applications with a total lending balance of NT$ 65.784 billion.

The SCSB finished setting up the sustainable investment sector in 2023 with a view to having stakeholders and investors acknowledge the concept of sustainable investment and the social impacts made by their investment decisions. Likewise, the SCSB also furnished an ESG-themed investment webpage where sustainable investment-conscious enterprises and individuals were welcomed to critically choose from ESG funds and overseas bonds. Lastly, there were a total of 7 listed funds meeting the Financial Supervisory Commission’s (FSC) ESG fund criteria in 2024 with an accumulated amount of 54 listed funds and the scale for AUM valued at NT$ 452 million in the same year.

Responsible Financing

The SCSB not only follows the “Equator Principles” and the “Principles for Responsible Banking (PRB)” but formulates the “Guidelines Governing SCSB’s Responsible Lending” , “Guidelines for Loans Applicable to the Equator Principles”, the “SCSB Sustainability-linked Credit Extension Guidelines”, and “Guidelines Governing Nature and Climate Risk Management” to review ESG risk factors deriving from lending applicants, investigate thoroughly negative sustainable information, and assess the potential impacts. Additionally, the extension of credit should take the following criteria into consideration, namely monitoring the status of credit applicants after granting loans, reviewing from time to time whether credit applicants fulfill their corporate social responsibilities, and proactively developing reactive plans for fear of credit applicants exerting potential negative sustainable impacts.

Project Financing

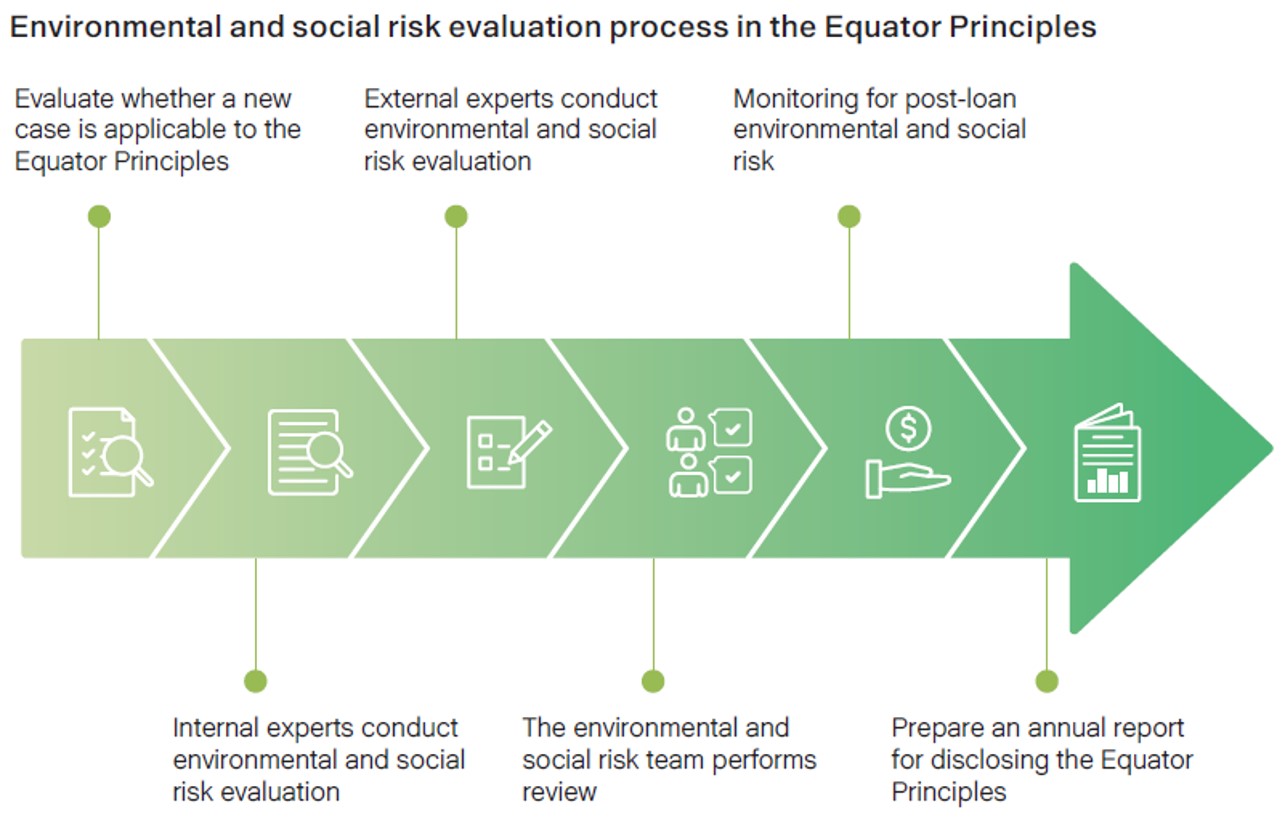

The SCSB’s project financing business complies with the requirements of “Guidelines for Loans Applicable to the Equator Principles”. Internal experts and independent third-party organizations evaluate the environmental and social risks of projects, categorizing them into three levels, namely A, B, and C. The evaluation includes human rights, climate change, GHG emissions, and biodiversity, as well as environmental and social management systems and plans to bolster and implement environmental and social risk management for project financing cases. In 2024, there were 4 accumulated cases applied to the Equator Principles and underwritten by the SCSB, of which 2 cases happened to be the same valid project finance information disclosed in 2023. Please find the detailed information below.

| Events | Affected environmental and social aspects | Management measures and results |

|---|---|---|

| Class C energy storage system- NT$ 4.1 billion and 8-year term syndicated loan |

|

|

| Class B solar fish farm- NT$ 15.8 billion and 3-year term syndicated loan |

|

|

| Class A wind power generation project-NT$ 62.475 billion and 16-year term syndicated loan |

|

|

| Class C solar fish farm- NT$ 7 billion and 5-year syndicated loan |

|

|

Green Building Loans

To encourage the public to purchase green buildings, the SCSB offers creditors with “Green Building Candidate Certificate”, “Green Building Label”, or “Smart Building Label” recognized by the Ministry of the Interior (MOI) to enjoy green building loans. In 2024, 832 loan applications were approved, with a balance at NT$ 10.1 billion.

Responsible Investment

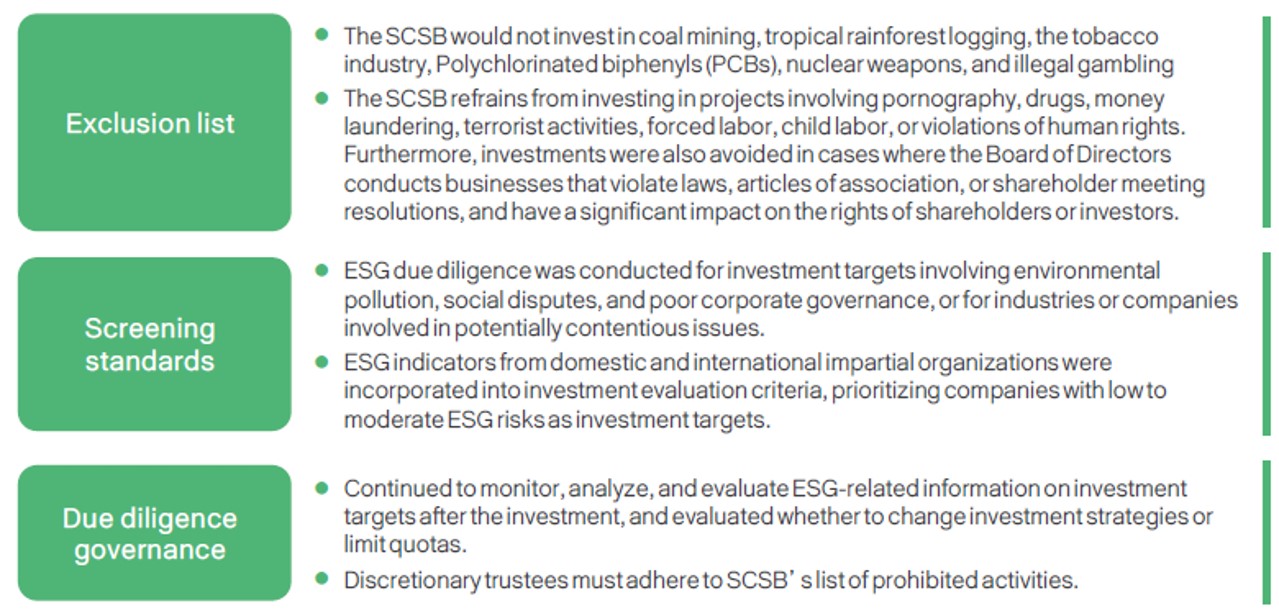

The SCSB follows the “Principles for Responsible Investment (PRI)” and the “Stewardship Principles for Institutional Investors” to formulate regulations such as the “Regulations Governing Responsible Investment”, “Regulations Governing Nature and Climate Risk Investment Management”, and “Stewardship Standards”, to dedicatedly develop green finance. In addition, through integrating ESG factors into investment decisions, promoting responsible investment and stewardship, and amplifying the sustainable influence within the financial services industry to foster a sustainable financial ecosystem. The discretionary asset management firms contracted by the SCSB have all signed statements of the “Stewardship Principles for Institutional Investors”, covering 100% of the environmental, social, and governmental risk in the investment process.

Sustainable Finance

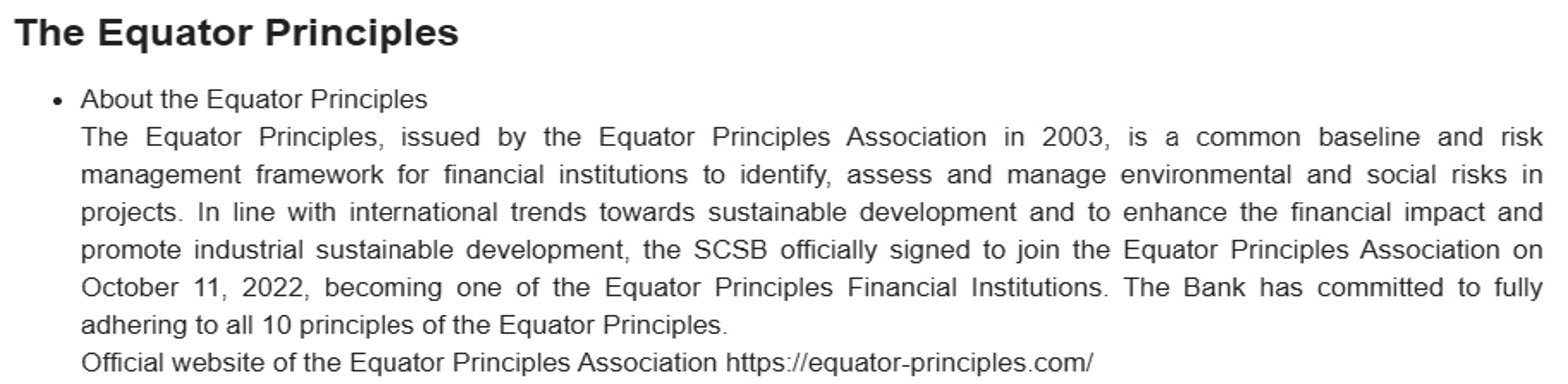

The SCSB works collaboratively with government guidelines, plans out products and services by resonating with the green finance aspect, and supports the development of diverse industries, including solar power, green tech, and key start-ups. In addition, as the Financial Supervisory Commission (FSC) has actively promoted the “Green and Transition Finance Action Plan” since 2024, the SCSB projects to advance both investing and financing business for the Six Core Strategic Industries and other green energy industries wholeheartedly to fulfill the goals of sustainable developments and net-zero emissions. Furthermore, the SCSB officially joined the Equator Principal Association back in October 2022 where the firm would adopt the “Equator Principles 4 (EP 4)”, proactively conduct potential environmental and social risk management targeting credit cases, empower business partners to fulfill their environmental protection goals and social responsibilities, as well as optimize the sustainable finance impact.

Sustainable Financing Policy

Corporate Finance

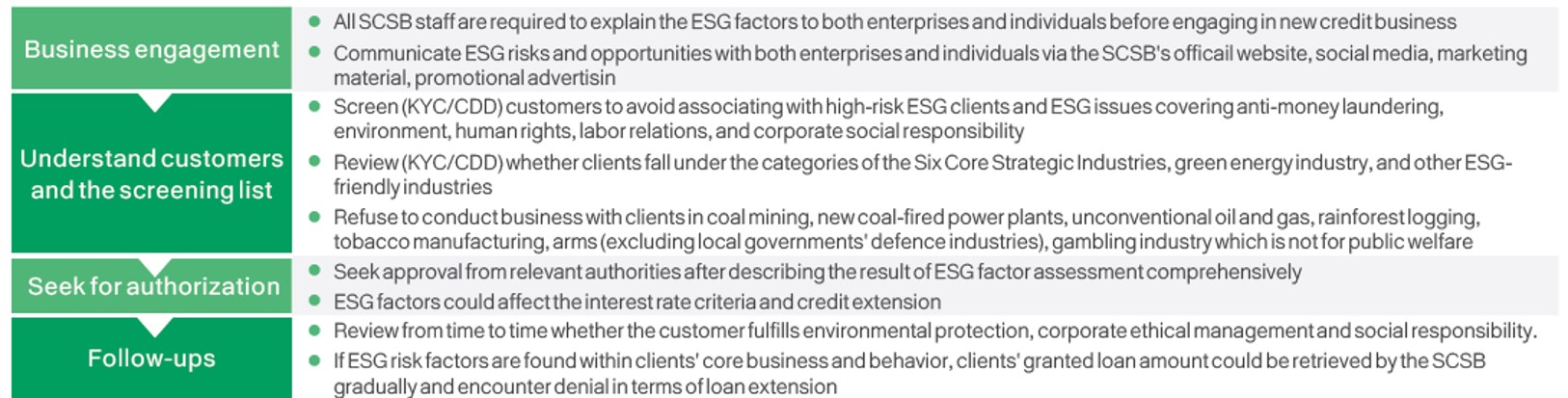

The SCSB incorporated ESG factors in its credit/lending business with corporate clients. As for ESG factors, they cover issues including anti-money laundering, environment, human rights, labor relations, and corporate social responsibility. Speaking of the KYC/CDD procedures, the SCSB screens clients to avoid engaging with high-risk ESG clients and ESG issues highlighted above. Moreover, a screening list of clients involved in coal mining, new coal-fired power plants, etc., are forbidden to engage with. Lastly, when it comes to engaging with clients on sustainability-linked risks and opportunities, the SCSB puts up internal guidelines and encourages corporate clients to achieve certain ESG indicators such as GHG emissions intensity, water consumption per unit of revenue, etc., to benefit from rate cuts in return. Likewise, the SCSB is sets to futhrer promote ESG-centric consultancy service in 2024 and assist SMEs in achieving low-carbon innovation development, offering infrastructure-centric project loans for factories categorized under government unregistered and certain factories.

Consumer Finance

The SCSB incorporated ESG factors in its credit/lending business with individuals. As for ESG factors, they cover issues including anti-money laundering, environment, human rights, labor relations, and corporate social responsibility. Speaking of the KYC/CDD procedures, the SCSB screens clients to avoid engaging with high-risk ESG clients and ESG issues highlighted above. Moreover, a screening list of clients involved in coal mining, new coal-fired power plants, etc., are forbidden to engage with. Additionally, the extension of credit should take the following criteria into consideration, namely monitoring the status of credit applicants after granting loans, reviewing from time to time whether credit applicants fulfill their corporate social responsibilities, and proactively developing reactive plans for fear of credit applicants exerting potential negative sustainable impacts. Finally, individuals are encouraged to visit SCSB’s website to acknowledge the concept of sustainable investment and the social impacts made by their investment decisions, fulfilling the view of engage responsibly with clients.

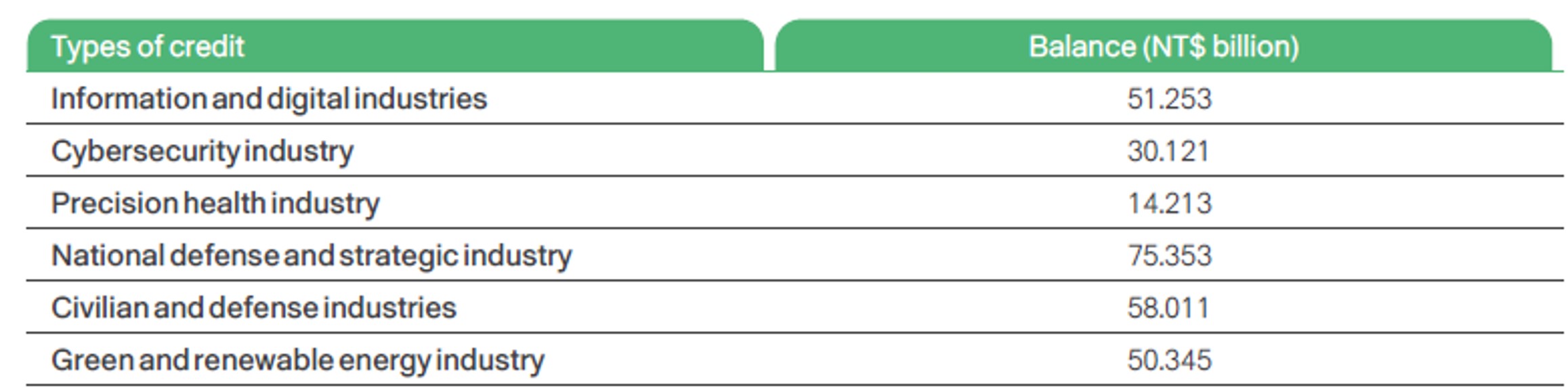

Credit Business with the Six Core Strategic Industries

The SCSB actively provides funds to the Six Core Strategic Industries, empowers economy transmissions, and aids in industry recovery. In 2024, there are 13,956 credit cases in total with the credit balance accounting for NT$ 145.853 billion.

Note: As the Six Core Strategic Industries contained double-counting ones, the balance amount applied to each column would not be consistent with the credit balance of the Six Core Strategic Industries.

Credit Business with Green Energy Infrastructure

To achieve the net-zero goal in 2050, the SCSB supports the development of green energy infrastructure and encourages customers to invest in the construction of solar power plants, wind power plants, and renewable energy systems and plants. By the end of 2024, there were 373 credit cases in total with the credit balance exceeding NT$ 5.038 billion.

Corporate Finance

In 2024, the total value of corporate lending was NT$ 542,945,000,000 while the total value of green loans and sustainability-linked ones was NT$ 39,366,000,000. Furthermore, speaking of SME-tailored sustainable financing. the SCSB assists SMEs in achieving low-carbon innovation development, offering infrastructure-centric project loans for both managed factories and specific ones, accounting for NT$ 6,222,000,000 while the amount for SME green credit and sustainable one stands for NT$ 6,508,000,000 and NT$ 2,256,000,000, respectively. This way, these three targets comprise of SME-tailored sustainable financing accounted for NT$ 14,986,000,000. Lastly, the percentage of total sustainable value over total value was at 10.01%.

Consumer Finance

In 2024, the amount of green building mortgage accounted for TWD 10,100,458,209, while the value for personal and mortgage lending was equivalent to NT$ 354,429,070,567. This way, the ratio for total sustainable value over total value was at 2.85%.

Sustainable Finance

The SCSB works collaboratively with government guidelines, plans out products and services by resonating with the green finance aspect, and supports the development of diverse industries, including solar power, green tech, and key start-ups. In addition, as the Financial Supervisory Commission (FSC) has actively promoted the “Green and Transition Finance Action Plan” since 2024, the SCSB projects to advance both investing and financing business for the Six Core Strategic Industries and other green energy industries wholeheartedly to fulfill the goals of sustainable developments and net-zero emissions. Furthermore, the SCSB officially joined the Equator Principal Association back in October 2022 where the firm would adopt the “Equator Principles 4 (EP 4)”, proactively conduct potential environmental and social risk management targeting credit cases, empower business partners to fulfill their environmental protection goals and social responsibilities, as well as optimize the sustainable finance impact.

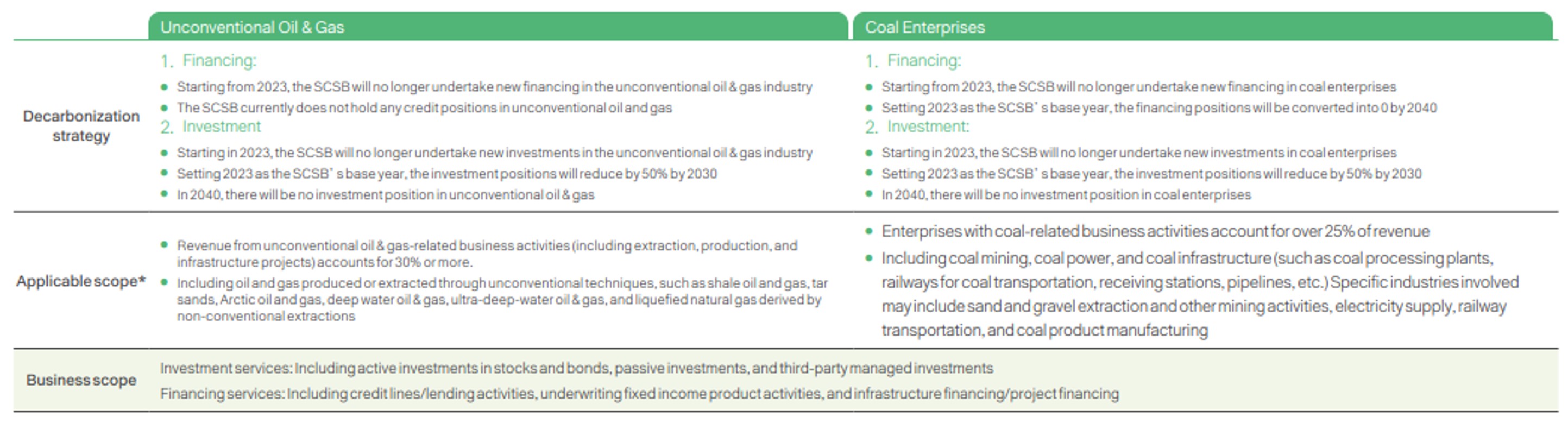

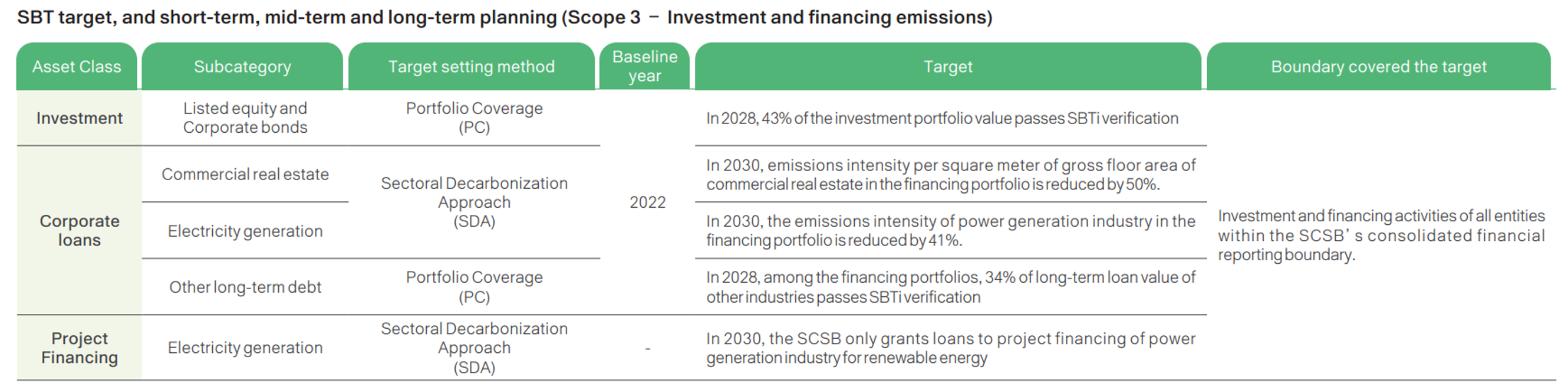

For investments and financing businesses involving high carbon-emitting fossil fuels, the SCSB has set the following phased reduction targets:

Note :The applicable scope does not include investments or financing for state-owned enterprises in different countries or funding for sustainable transition purposes.

Climate and Nature-related Information

According to the Global Risks Report 2025 from the World Economic Forum (WEF), climate change and environment-related risks remain among the most serious global threats in the next decade, including extreme weather events, critical disruption in Earth system, biodiversity loss and ecosystem collapse, natural resource shrotage, and pollution. Addressing the impacts of climate change has become a shared global imperative. In recent years, governments worldwide have intensified regulatory efforts, and set net-zero carbon targets to strengthen their climate resilience strategies. Taiwan has also legislated its 2050 Net-Zero Emissions Target, and additional climate-related regulations for industry sectors are expected, presenting both risks and opportunities for enterprises. In response to the growing climate-related risks and opportunities, the SCSB continued to align with the Financial Supervisory Commission’s Guidelines for Climate-related Financial Disclosures for Domestic Banks. In 2024, the Board of Directors revised the SCSB’s "Guidelines Governing Nature and Climate Risk Management", aiming to identify and assess material nature- and climate-related risks and opportunities across our operations. This effort strengthens the SCSB’s governance, strategy, and risk management in addressing environmental issues. The SCSB also establish metrics and targets to regularly monitor implementation progress, supporting the SCSB’s ongoing response to stakeholder concerns regarding the SCSB’s nature and climate resilience.

Governance

The Board of Directors at the SCSB serves as the highest governance body for natural and climate change-related issues, bearing ultimate responsibility for decision-making and oversight. A Risk Management Committee is established under the Board to assist in reviewing the effectiveness of nature- and climate-related management and strategic planning. In addition, the SCSB and executive departments have established a Risk Management Committee and a Sustainable Development Committee, which are required to regularly submit reports and management recommendations to the Board. These efforts support the Board in effectively formulating and refining policies and procedures for managing nature- and climate-related risks and opportunities, thereby strengthening the overall governance framework.

The SCSB has established the “Guidelines for Natural and Climate Risk Management,” which clearly define the responsibilities of each management unit.

- Risk Management Committee: Authorized by the Board of Directors, the committee shall exercise the duty of care of a prudent manager and conduct at least an annual review of nature and climate risk issues. It is also responsible for submitting related recommendations and reports to the Board.

- Asset and Liability Management Committee: Responsible for reviewing the nature and climate risk-related regulations submitted by the Risk Management Department and examining the credit and investment portfolios to ensure that the financial risks associated with changes in natural capital or climate change are in compliance with the SCSB’s nature and climate risk management policies.

- Sustainable Development Committee: Responsible for reviewing strategies, risk management, indicators, and targets related to nature and climate issues, and for regularly tracking implementation status. The Sustainable Development Committee holds quarterly meetings and reports at least once a year to the Audit and Sustainability Committee on the progress of nature and climate-related strategic targets.

The Sustainable Development Committee chaired by the President acts as the consolidating and guiding unit for the SCSB´s sustainability development and natural and climate risk management. The committee convenes quarterly meetings to review the outcomes of climate-related policies, regulations, risks, and opportunities. The responsibilities of the two climate risk-related groups are as follows:

- Environmental Sustainability Team:Led by the Risk Management Department and the head of the department. This team is responsible for overseeing changes in nature capital and climate change-related issues, coordinating with various business units to identify risks and opportunities, and implementing action plans related to nature capital and climate change and environmental protection response measures. This ensures that nature and climate risks are adequately identified, managed, and addressed when conducting transactions or providing funding to clients in highly nature-sensitive or climate-sensitive industries.

- Responsible Finance Team:Led by the Treasury Department and the head of the department.This team is responsible for promoting the sustainable development of credit extension standards, green finance, responsible investment, and other relevant businesses, as well as implementing due diligence governance. This ensures that the SCSB maintains a strong foothold in the capital market and gradually establishes its leadership in the field of sustainable finance.

The Risk Management Department to gather and summarize the information and reports on nature and climate risks provided by each responsible unit at the end of the previous year. These reports are to be submitted to The Sustainable Development Committee on an annual basis. After consolidating and analyzing this information, the Risk Management Department must report relevant nature and climate risk information to the Board of Directors at least once a year. Additionally, the Risk Management Department compiles response measures developed by the respective units, enabling the Board of Directors and senior management to incorporate these considerations into their strategic planning and business monitoring.

Apart from the above mentioned top management units, other management units of the SCSB are responsible for assisting in system implementation, talent training, measuring, monitoring, and reporting nature and climate risks according to their respective business functions. They are also required to draft system requirements, request the Information Technology General Department to build databases, provide nature and climate assessment-related data and results, and collaborate with the implementation of nature and climate action within the SCSB. Furthermore, other units such as the business management units, the operations unit and Auditing Department, operate under the SCSB's "Practical Guidelines for the Three Lines of Defense in Internal Control". Each unit carries out its duties based on its respective business functions to identify and assess nature and climate risks and opportunities relevant to the SCSB, and formulate nature-related and climate-related strategies and measures (including nature-related and climate change-related risks and opportunities), establish mechanisms and processes for nature and climate risk management to enhance risk management, help the Risk Management Department perform bank-wide climate change scenario analysis and support the implementation of climate actions.

- Professional Competency Training for the Nature and Climate Risk Management Unit:

To ensure that the SCSB´s nature and climate risk management unit is equipped with the necessary capabilities to identify and respond to climate risks and opportunities effectively, themed training sessions and education are conducted annually for members of the Board of Directors and top management. The training aims to endow them with the knowledge and skills required to gain insight into international trends related to nature and climate change and sustainable operations. (For detailed information about nature and climate change education and training, please refer to 1.4 Risk Management and 3.2 Employee Training and Career Development). - Incorporation of Sustainability and Climate-related Management Incentives management measures:

The rewards and performance of the SCSB´s top management are evaluated based on the achievement of performance and work targets. The work targets include sustainability and climate development goals, which were formulated based on the annual work priorities planned by the SCSB´s six major working groups and the SCSB´s "Sustainable Strategic Target Planning". In 2024, the SCSB included the goals of “completing the GHG inventory, verification, and disclosure in time,” “introducing the IFRS S1 and S2 Sustainability Disclosure Standards,” “submitting the SBT carbon reduction target as required by the SCSB, and execute the carbon reduction pathway in time,” and “fulfilling the commitment to energy resource reduction target, and executing the carbon reduction pathway in time” into the KPI of the President and the Senior Executive Vice President, accounting for 6% of their overall performance evaluation. (Please refer to 1.1 Corporate Governance for sustainability and climate-related KPI information).

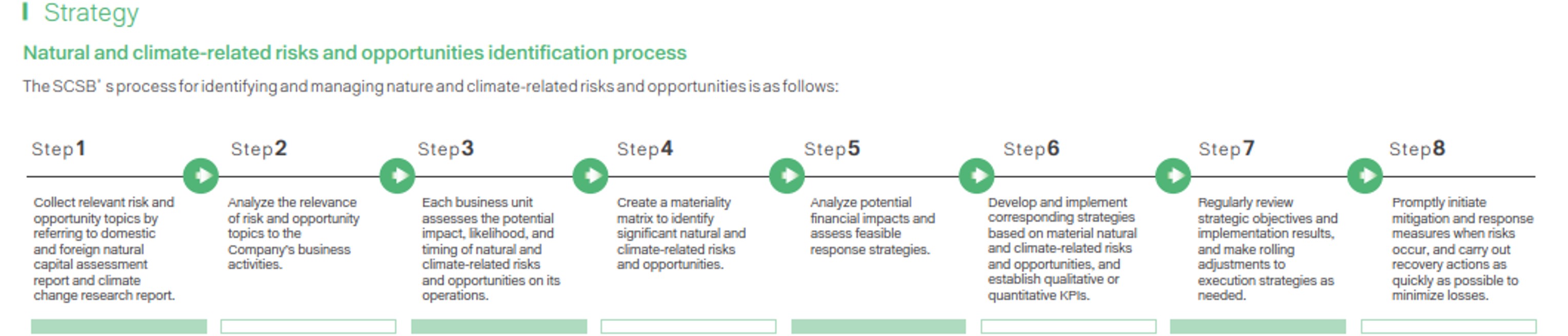

Strategy

Natural and climate-related risks and opportunities identification process

The SCSB’s process for identifying and managing nature and climate-related risks and opportunities is as follows:

The SCSB formulates nature- and climate-related risk and opportunity issues annually and submits corresponding recommendations and reports to the Board of Directors. Every two years, each department conducts a regular identification of nature- and climate-related risks and opportunities to ensure that major decisions can take into account timely changes in both internal and external environments and trends.

When assessing nature- and climate-related risks and opportunities, all departments must follow consistent evaluation standards and definitions. Assessments are based on the likelihood of occurrence, impact level, and expected time of occurrence to ensure the objectivity and comparability of the results.

The scope of impact is defined across the value chain as upstream (suppliers), midstream (the SCSB’s operations), and downstream (clients and consumers). The time horizon is categorized as short term (within 1 to 3 years), medium term (3 to 5 years), and long term (more than 5 years).

Likelihood of occurrence and impact level are also key indicators, both assessed using a five-level scale: High, Moderately High, Medium, Moderately Low, and Low.

All departments are required to comprehensively consider the potential negative impacts of risks or the benefits of opportunities, along with their likelihood of occurrence, and analyze the resulting effects on business operations and financial performance.

Upon completion of the evaluation, the SCSB prioritizes risks and opportunities based on their level of impact, and determines the material nature- and climate-related risks and opportunities after consideration of the associated trade-offs.

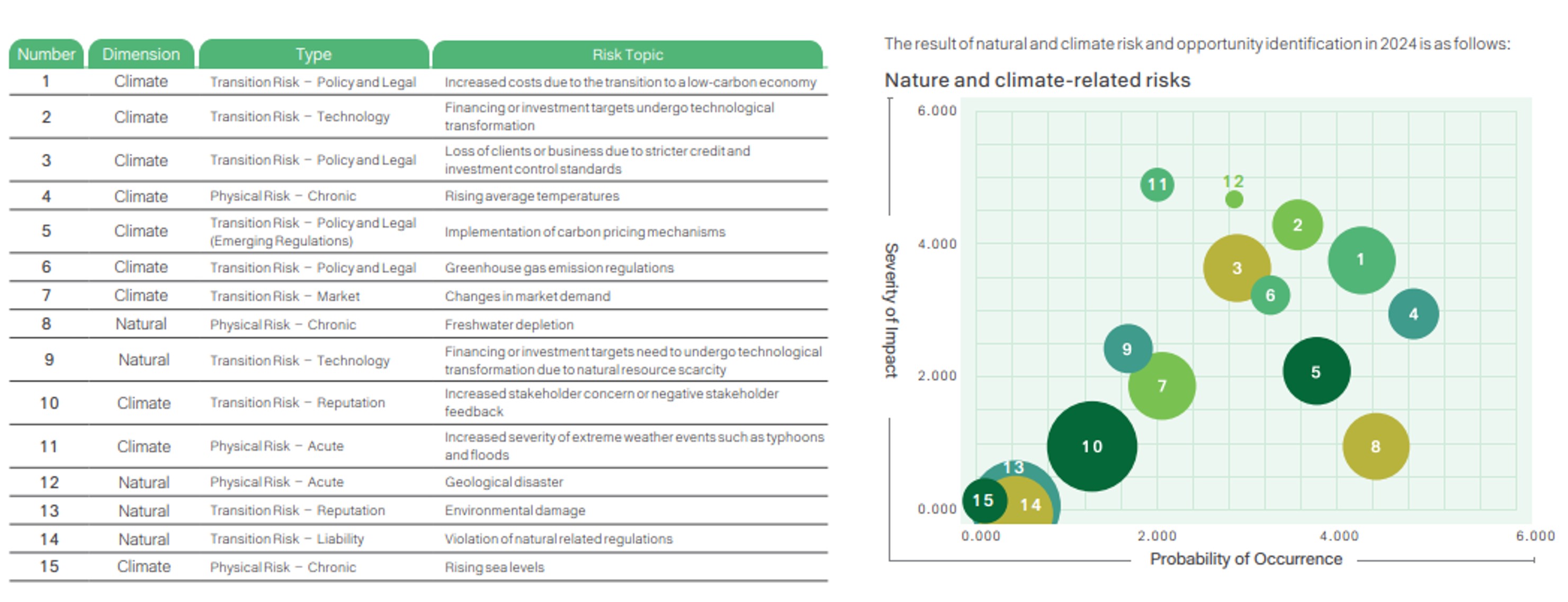

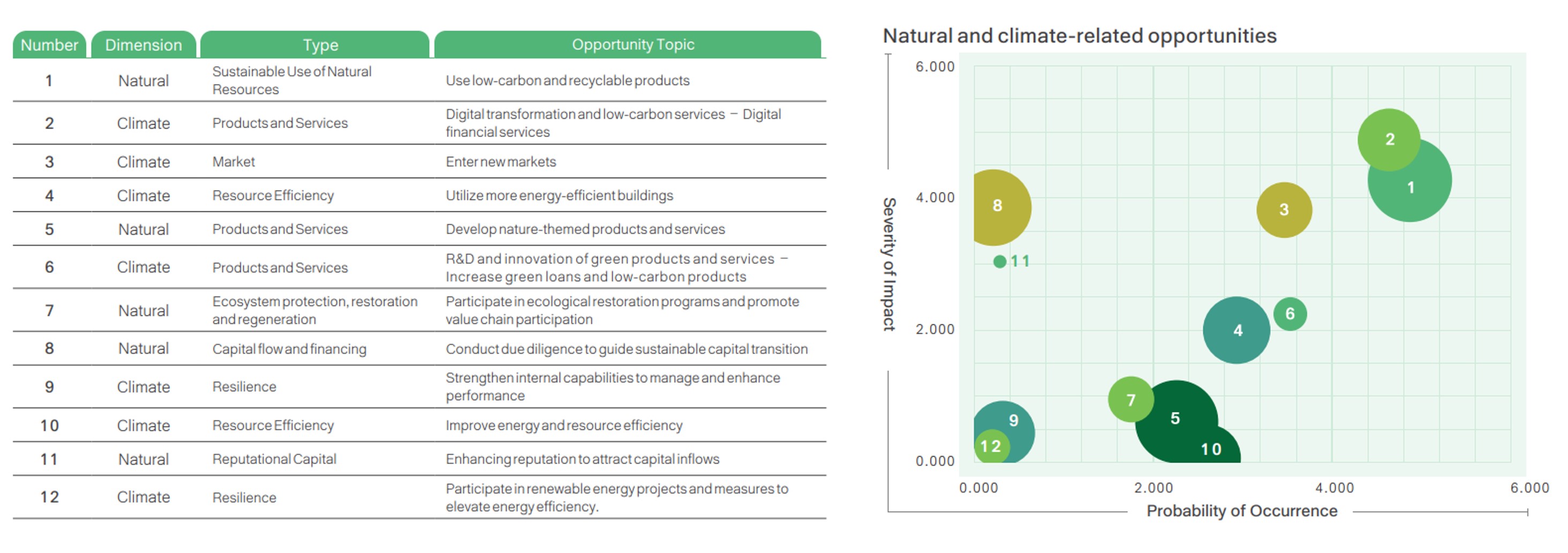

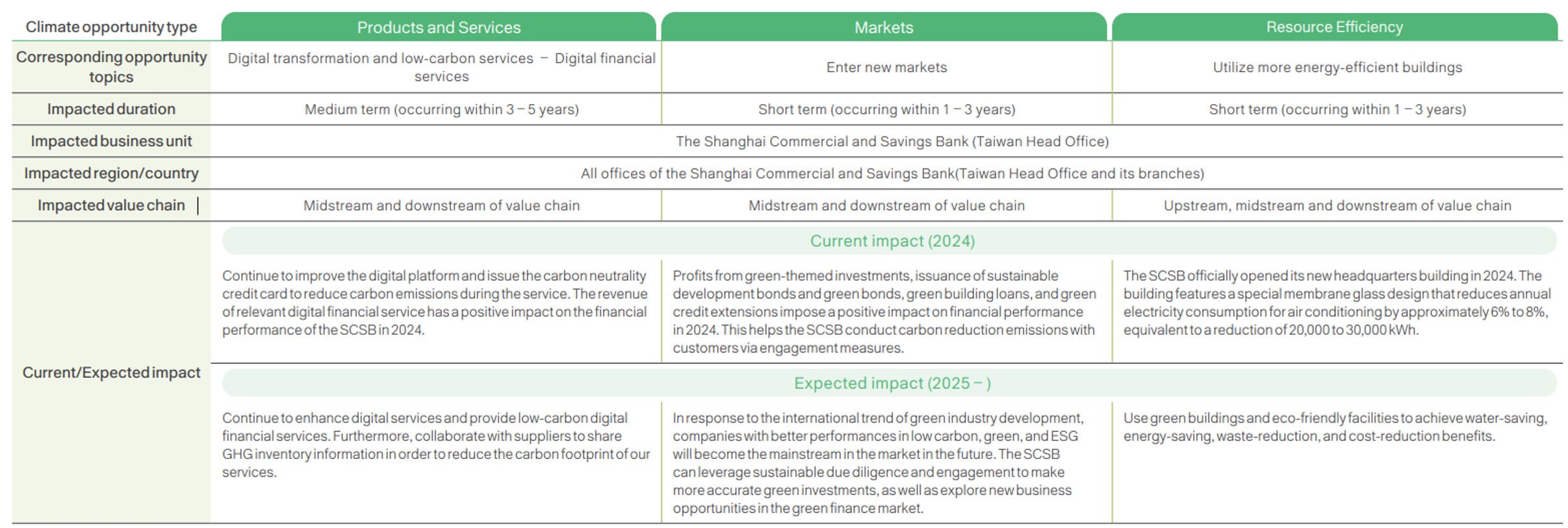

The result of natural and climate risk and opportunity identification in 2024 is as follows:

Nature and climate-related risks

Natural and climate-related opportunities

Impacts and Strategies for Risks and Opportunities

For identified critical nature and climate topics, corresponding response strategies and targets are formulated, and qualitative or quantitative KPIs are set to ensure that the management mechanism is concrete, measurable, and trackable. In addition, the SCSB monitors the progress of relevant strategies year by year, and checks how the financial resource is invested in and target achievement. In the meantime, the SCSB conducts rolling adjustments based on the operating development to increase operational resilience and the effectiveness of risk management.

The following section outlines the SCSB’s assessment of the impacts posed by major nature- and climate-related risks and opportunities identified for the year, along with the corresponding response strategies.

Risk impact:

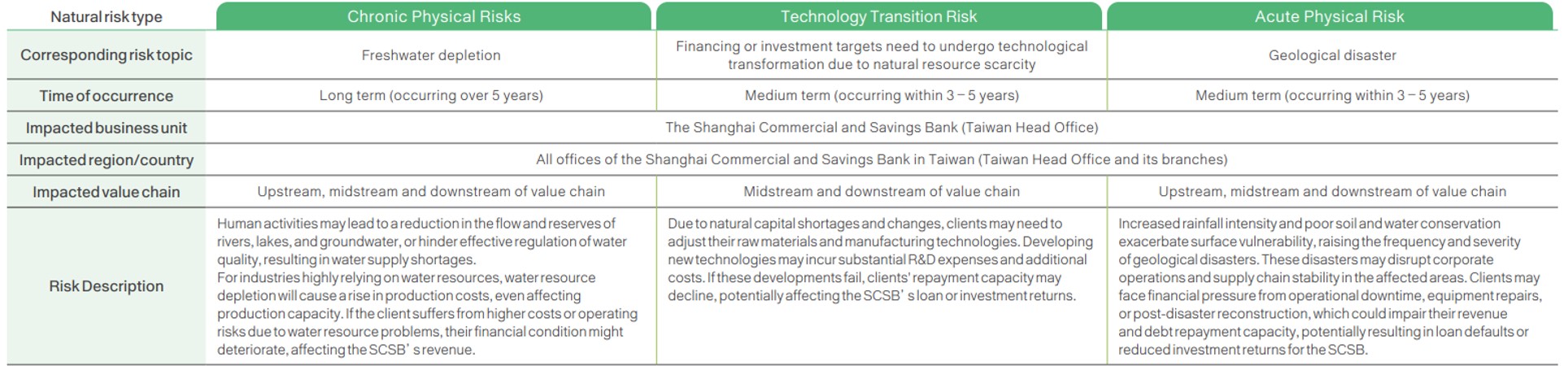

Material nature risk impact:

Material climate risk impact:

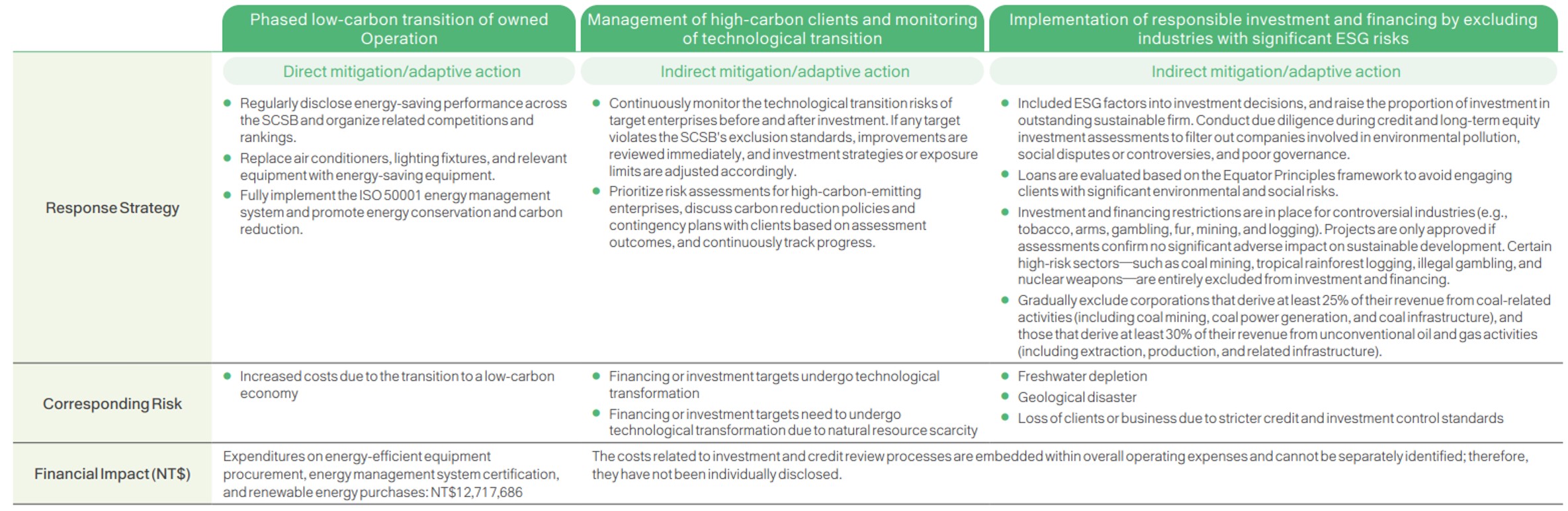

Material nature and climate risk response strategies

Note : Part of the risk response measures above have been integrated with the SCSB’s GHG reduction strategy. For detailed corresponding targets and short-, medium-, and long-term strategic planning, please refer to Chapter 2.3 Green Operation.

Material nature opportunity impact:

Material climate opportunity impact:

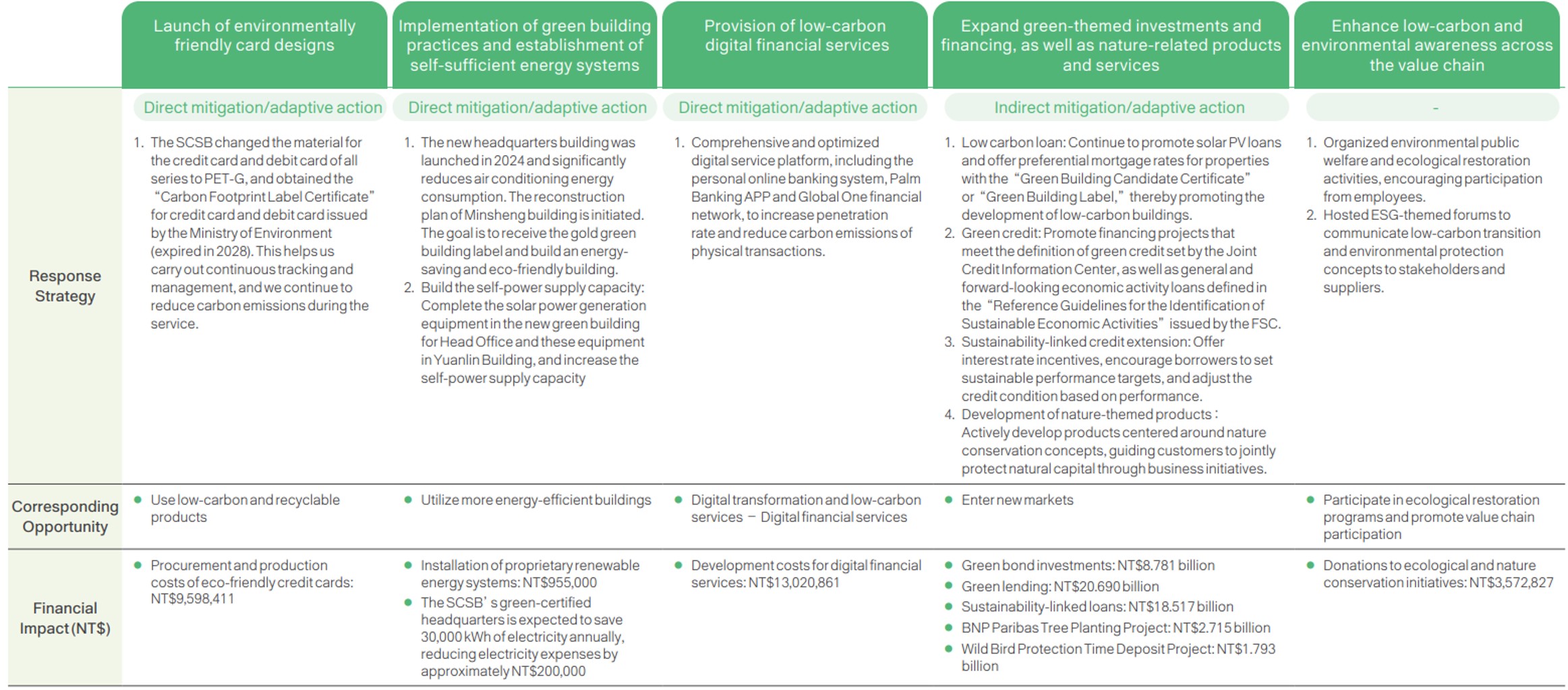

Natural and climate opportunity response strategies

Note 1: Financial impact items include operating expenses, donation expenditures, other indirect items (such as entrusted assets), and estimated amounts.

Note 2: The aforementioned opportunity response measures have been integrated into the SCSB’s GHG reduction strategy. For detailed corresponding targets and short-, medium-, and long-term strategic planning, please refer to Chapter 2.3 Green

Operation.

Summary of financial impact associated with risk and opportunity

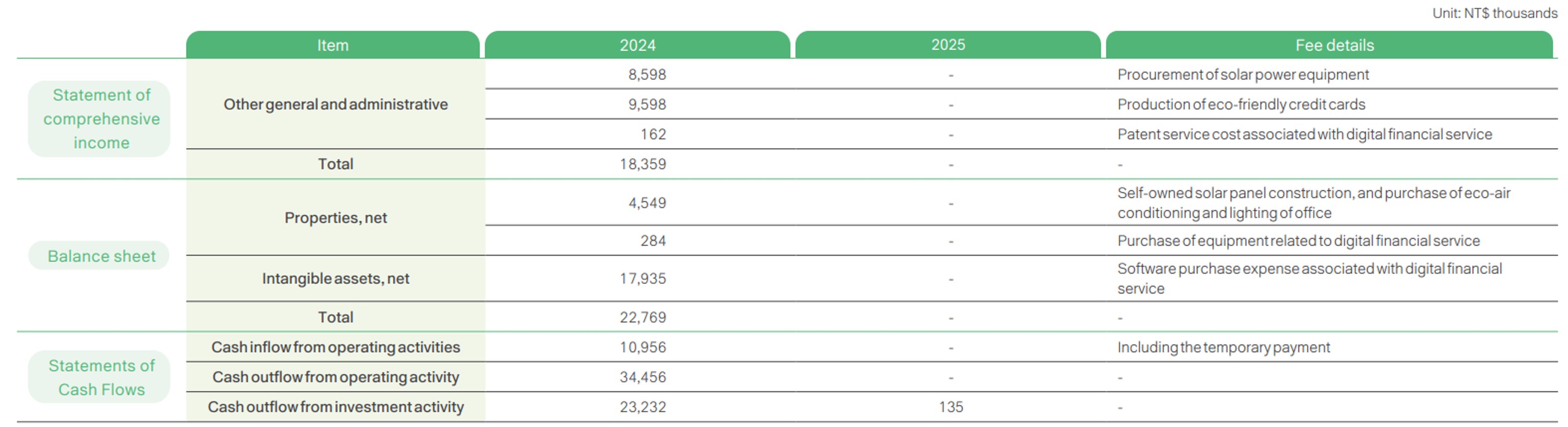

To strengthen risk management and assess the allocation or impact of financial resources, the SCSB has preliminarily identified the direct financial impacts arising from critical risks and opportunities, as well as the related expenditures and amounts resulting from corresponding response strategies. These items have been mapped to relevant accounting line items in the income statement, balance sheet, and cash flow statement, enabling clearer identification of how material risks and opportunities may affect the SCSB’s financial position, performance, and cash flows.

Direct impact of climate risks and opportunities on short-term, mid-term and long-term financial condition, financial performance and cash flow

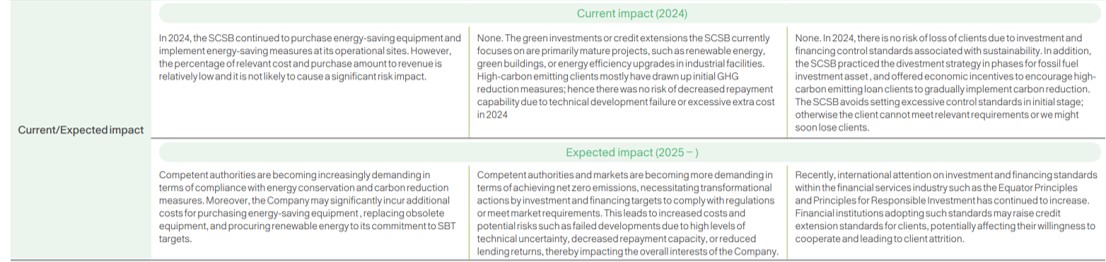

- Short term (1 to 3 years): In 2024, to support its low-carbon transition plan, the SCSB invested in energy-saving equipment, green energy purchases, and the construction of a solar power generation system. These expenses were recorded under other business and management costs for the current period, affecting financial performance and leading to increased cash outflows from operating activities. However, the associated amount has a limited impact relative to the overall scale of the SCSB’s operations and is not expected to have a significant effect on short-term financial condition, performance, or cash flow.

- Mid term (3 to 5 years): Purchase of energy-saving equipment and green energy is continuous expenditure. The SCSB entrusted a professional agency to assess a proper location for solar power generation system and organized the budget. It is expected that the impact on financial condition, financial performance and cash flow will be equivalent to the case in the short run.

- Long term (5 years and above): Due to the extended timeframe, it is difficult to accurately assess the actual impact of climate-related risks or opportunities on long-term financial performance. Moreover, any existing assessments may have limited reference value; thus, no conclusive evaluation is currently available.

Impact of relevant response strategies on short-term, mid-term and long-term financial condition, financial performance and cash flow

- Short term (1 to 3 years): To grasp the business opportunity of digital finance and launch the low-carbon service, the SCSB actively develops the mobile app and online financial service, incurring the expenditure of software purchase, patent expenses, and credit card production expenses. These expenses are included in other business and management expenses of the current period. They affected the short-term financial performance, causing the increase in cash flow of operating activity. The aforementioned expenditure has a limited impact on the overall operational scale of the SCSB. It is expected that it has no significant impact on financial condition, financial performance, or cash flow in the short run. In addition, this strategy supports the development of the SCSB’s digital finance and low-carbon services, laying the foundation for future business growth.

- Mid term (3 to 5 years): The technologies adopted by digital financial service are mostly mature. It is possible to estimate the usage fee or development fee of relevant patent and software rationally. In addition, to respond to market needs instantly, the SCSB has purchased sufficient eco-friendly credit cards to reduce the cost of credit card production in future. Therefore, it is expected that relevant response measures will not have any major impact on financial condition, financial performance or cash flow in the mid run.

- Long term (5 years and above): The SCSB expects to continue with the existing response strategy, and makes adjustments in time, depending on the climate change trend, market need and technological development. However, the long-term strategy might be adjusted due to external environmental changes; now it is hard to assess its impact on financial condition precisely. In the future, the SCSB will continue to pay attention to the situation and adjust response plans dynamically

Risk Concentration and Resilience Analysis

Climate Scenario Analysis

To reflect the impact of climate risks on the SCSB, a scenario analysis is conducted to assess the severity of potential impacts on each business area in the event of physical climate risks and transition risks. The SCSB used the “Representative Concentration Pathways” (RCPs)(Note 1) from the Assessment Report 5 (AR5) of the Intergovernmental Panel on Climate Change (IPCC) to project the climate scenario. The scenario analysis will help the SCSB to develop appropriate risk management strategies and responses to potential impacts, to enhance its climate resilience.

Note 1: The Fifth Assessment Report (AR5) of the IPCC introduced four Representative Concentration Pathways (RCPs): RCP 2.6, RCP 4.5, RCP 6.0, and RCP 8.5, which represent increases in radiative forcing by 2100 of 2.6, 4.5, 6.0, and 8.5 watts per square meter, respectively. In 2021, the IPCC released its Sixth Assessment Report (AR6), which introduced Shared Socioeconomic Pathways (SSPs), incorporating socioeconomic development factors into climate scenario design. These SSP-based scenarios are not yet included in this report.

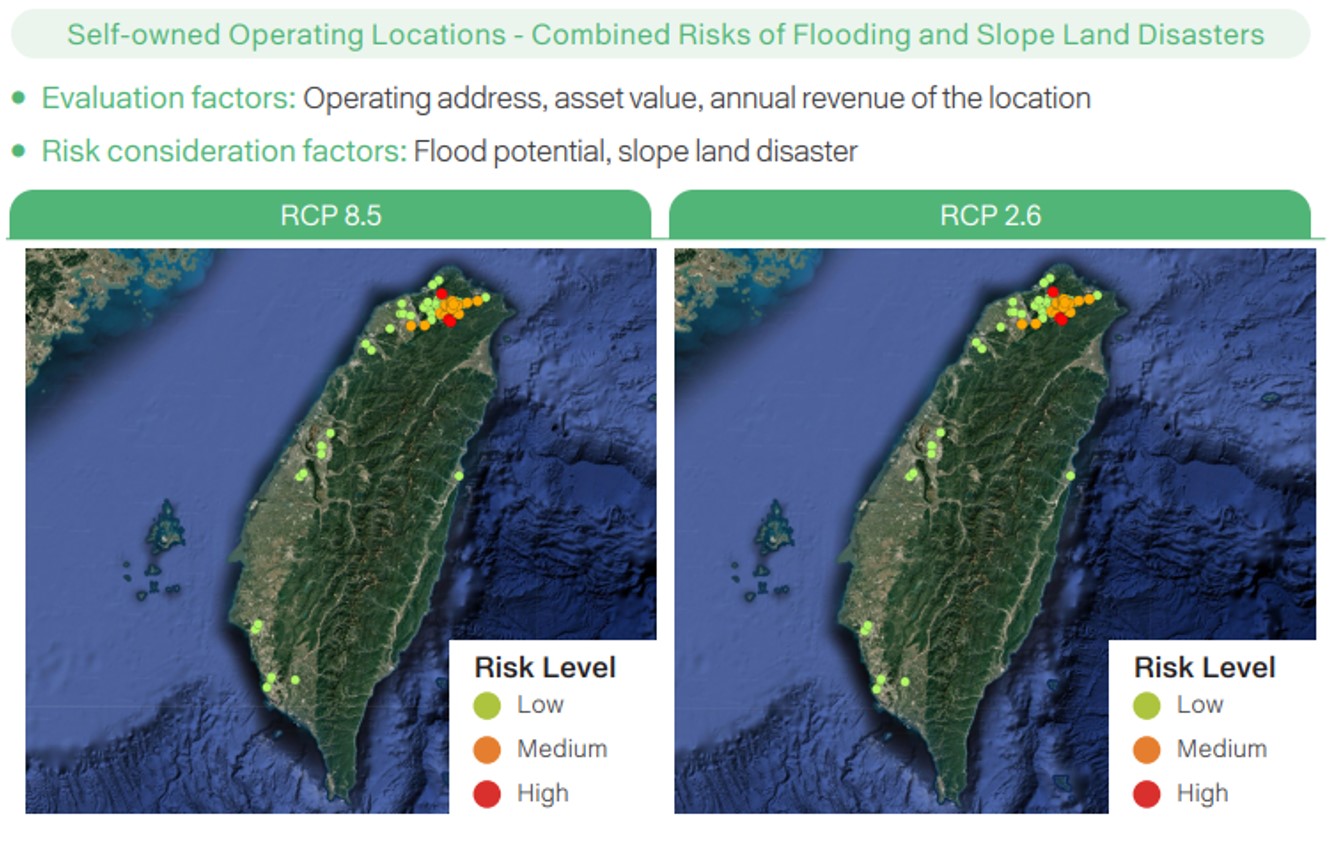

Scenario Analysis of Self-owned Location

To understand the possible impacts of physical risks on the SCSB’s site assets , the SCSB conducts a physical risk assessment for each business locations. The SCSB utilizes a risk sensitivity map based on physical risk severity levels of 1 to 3 (extreme rainfall frequency within 24 hours), vulnerability levels of 1 to 10 (flood potential, slope disasters), and exposure levels of 1 to 10 (exposure amounts). Using RCP 8.5 and RCP 2.6 as the hypothetical scenarios for risk impact, a risk analysis of the SCSB´s assets was carried out for the mid-century period (2036–2065), and corresponding climate risk management strategies were also proposed.

Note :The exposure amount is determined by evaluating the combined asset value and revenue of each location.

Analysis Outcome of Self-owned Locations

The SCSB conducted a climate sensitivity analysis at 74 of its locations in Taiwan. The analysis was performed under the most severe conditions of RCP 8.5, and the results showed that none of the locations were highly sensitive, 10 (13.51%) were categorized as medium-sensitivity locations, while the remaining 64 (86.49%) were considered low-sensitivity locations , including 44 locations (59.46%) with a risk sensitivity value below 50. When the Value of the SCSB premises under risk scenarios, the SCSB's total exposure to physical risks is approximately 5.10% of the total asset value of its locations, the exposure value of mediumsensitive locations is approximately 3.18% of the total asset value of all locations, and the exposure value of low-sensitivity locations (including locations with a sensitivity of 1 to 100) represents approximately 1.92% of the total asset value of all locations

Note :The scenario assumptions are based on flood potential assessment maps released by the National Science and Technology Center for Disaster Reduction (NCDR) via the Disaster Risk Adaptation (Dr.A) Platform. These maps incorporate simulations that account for Taiwan’s rainfall patterns, topography, and flood potential.

Before implementing any management measures, the risks driven by changes in physical climate parameters or other climate-change related developments were assessed based on scenario analysis. Under the“RCP 8.5”scenario in 2036, if SCSB’s owned operations were disrupted due to climate hazards such as landslides or flooding, the estimated financial impact in terms of revenue and asset damage would amount to NT$1,140,337,500.

To mitigate the impact of physical risks, the SCSB has developed a phased low-carbon transition plan for its owned operations, aiming to help slow the pace of global warming. The plan includes the adoption of energy-efficient equipment, the verification of energy management systems, and the expansion of renewable energy use. The estimated cost of implementing these management measures is NT$12,717,686.

Response Strategy and Climate Resilience Evaluation

According to the analysis results, the SCSB´s operating locations in Taiwan are not exposed to significant physical risks. However, to ensure effective control of the impact of physical risks, various operating locations have established response plans and disaster prevention protocols, as well as data backup readiness to minimize the damage of short-term natural disasters and maintain operational continuity in the aftermath of disasters.

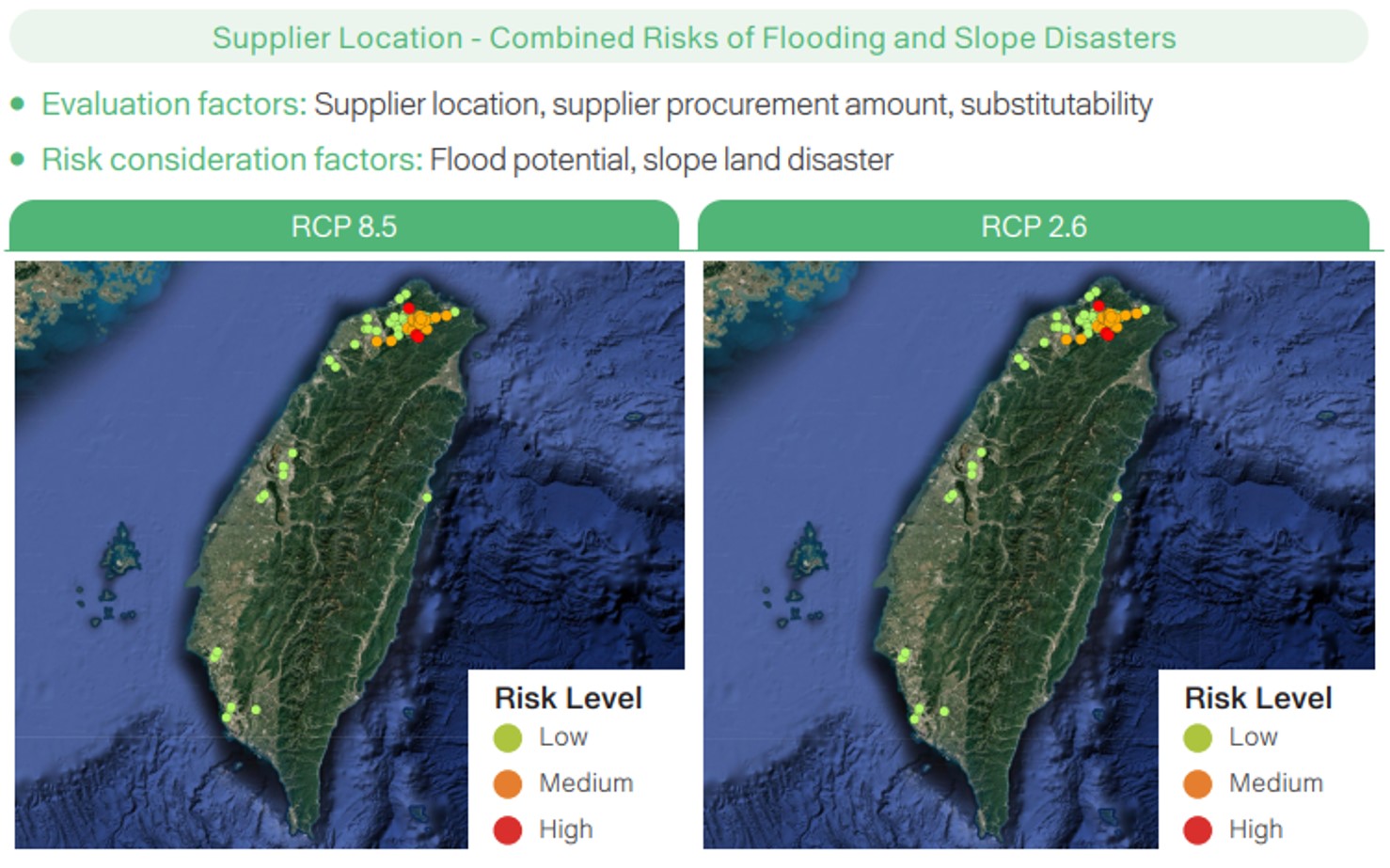

Scenario Analysis of Supplier Locations

The SCSB used RCP 8.5 and RCP 2.6 as the hypothetical scenarios for risk impact, taking into consideration the combined risks of flood potential and slope land disaster, categorizing climate sensitivity into three levels: high, medium, and low. A higher climate sensitivity represents a greater threat of climate disasters. Based on this, an analysis of the exposure situation for 198 suppliers in Taiwan for the mid-century period (2036–2065) was conducted in 2024.

Note: The scenario assumptions are based on flood potential assessment maps released by the National Science and Technology Center for Disaster Reduction (NCDR) via the Disaster Risk Adaptation (Dr.A) Platform. These maps incorporate simulations that account for Taiwan’s rainfall patterns, topography, and flood potential.

Analysis Outcome of Supplier Locations

According to the scenario evaluation under the condition of RCP 8.5, most of the SCSB´s 195 suppliers have medium to low climate sensitivity. Together, they accounted for 99.47% of the SCSB´s overall procurement amount in 2024. There were only three suppliers with high climate sensitivity, accounting for 0.53% of the procurement amount.

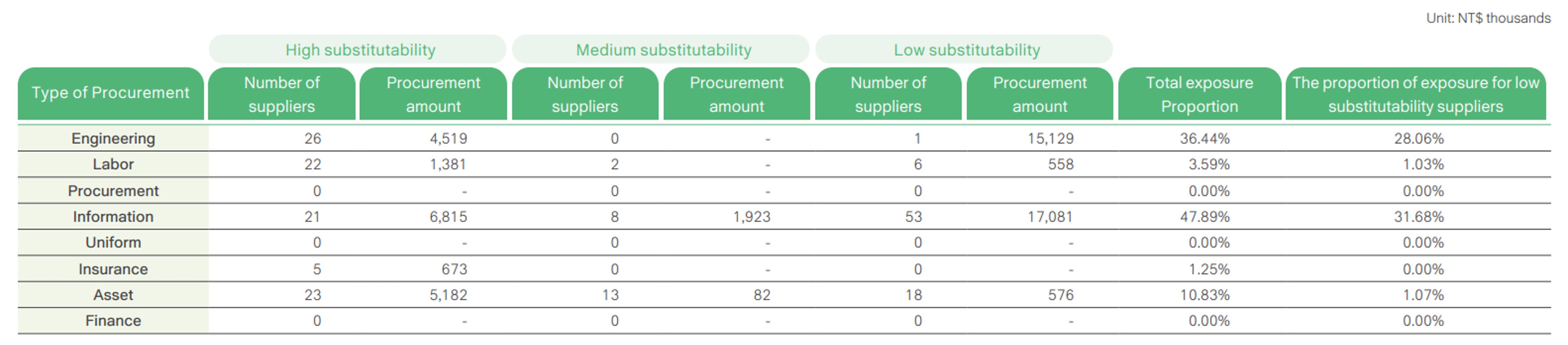

In addition, to understand the impact of physical risks on suppliers, the SCSB assessed how different types of suppliers were affected by physical risks under the RCP 8.5 scenario. The SCSB also performed substitutability analyses on various suppliers, which were categorized into three levels, namely high substitutability (other suppliers can be found within a month), medium substitutability (other suppliers can be found within three months), and low substitutability (other suppliers can be found more than six months). Suppliers classified as low substitutability are primarily concentrated in the information technology and engineering categories, accounting for 61.84% of the exposure.

Most of the SCSB’s IT and engineering suppliers are long-term partners. Although similar vendors are not scarce or difficult to find, these suppliers are generally categorized as low substitutability due to established working relationships and the need for operational continuity, resulting in a higher proportion. A review of these suppliers’ climate risk sensitivity shows that most fall within the medium to low risk range. Overall, the SCSB's internal assessment indicates that the impact of supplier-related risks remains limited.

To further enhance resilience, the SCSB has established a list of potential alternative vendors for suppliers with low substitutability, enabling prompt engagement and collaboration in the event of supply disruptions caused by unexpected climate-related events.

Note :The exposure amount is the procurement value that could potentially be affected on suppliers if the assumed risk occurs.

Response Strategy and Climate Resilience Evaluation

Although the current assessment reveals that the supply chain has negligible impact on operations, the SCSB will continue to monitor the stability of supplier delivery and vigorously find new suppliers to improve substitutability. Furthermore, to enhance the climate risk preparedness of suppliers, the SCSB will host supplier conferences to promote climate risk prevention measures and disaster relief knowledge, and advise high-risk suppliers to install flood control equipment.

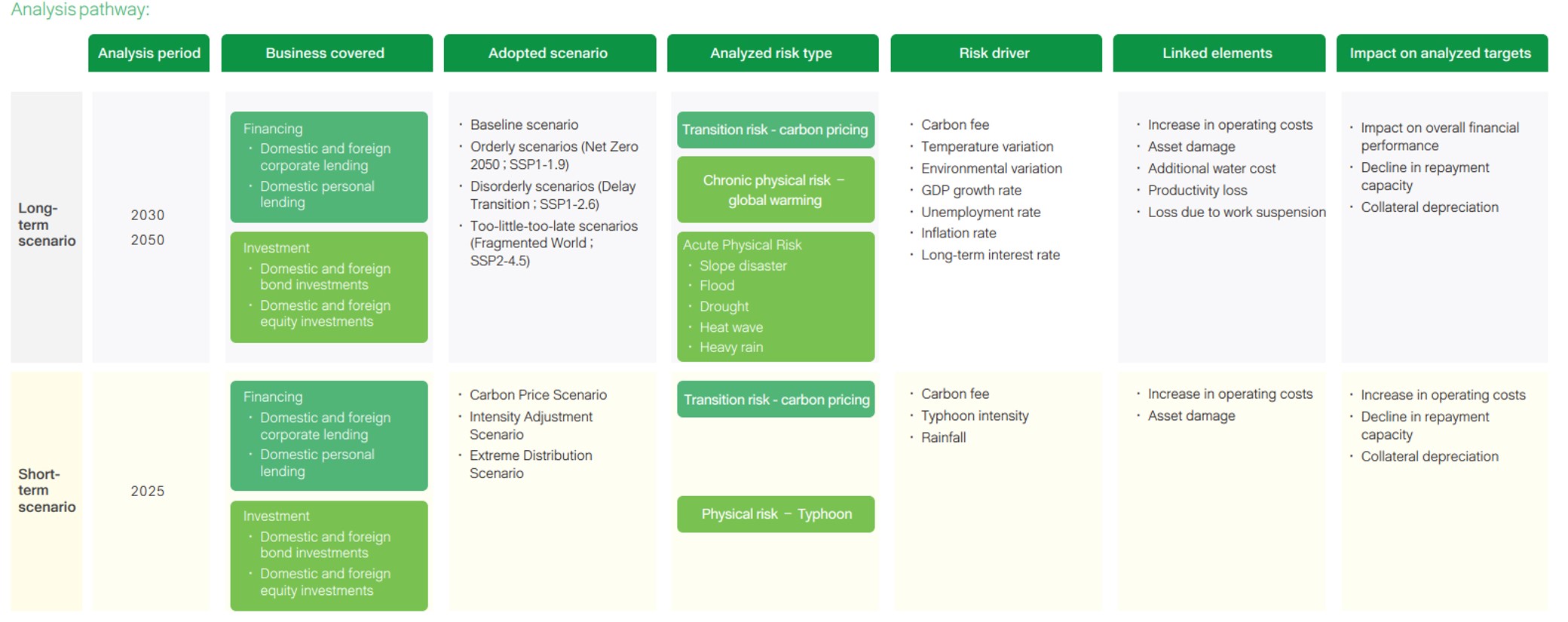

Scenario Analysis of Lending and Investment Portfolios

To ensure objective evaluation and continually monitor the impact of climate change risks on business and operations, the SCSB abides by the “Planning for Climate Change Scenario Analysis by Domestic Banks” (hereinafter referred to as the “operational plan”). The SCSB analyzes the potential long- and short-term risk impacts on bankbook positions — including domestic and foreign credit, bonds, and equity investments — as of the end of 2024, under various climate scenarios.

The SCSB referred to the methodology outlined in the operational plan, employing macroeconomic pathways (e.g. GDP, bank lending rates, inflation rates, and unemployment rates) and microeconomic pathways (including revenue losses, collateral losses, and additional costs) to conduct a comprehensive analysis. Furthermore, the SCSB incorporated a probability of Recovery Given Default estimation model to carry out the valuation. Therefore, the SCSB assesses financial resilience of the client in different climate scenarios, further assesses the potential impact of changes in loan repayment ability and collateral value on credit risk and revenue.

Note1:The expected losses under each scenario are subject to inherent uncertainties and do not represent actual future outcomes. Caution should be exercised when using or interpreting the analysis results, given their limitations.

Note2:The scope of analysis is based on the SCSB’s individual entity, including the operations of both domestic and overseas branches as well as offshore banking unit(OBU).

- Long-term scenario: Evaluate the long-term impacts of climate change and banking business cycles through both macroeconomic and microeconomic pathways. The time for analysis is 2030 and 2050.

- Short-term scenario: Based on a microeconomic pathway, the analysis focuses on potential climate events that may occur within the next year. The time point for analysis is 2025.

The scenario analysis method and assessment result are as follows:

Long-term scenario

The long-term scenarios include Current Policies (baseline), Orderly, Disorderly, and Too-little-too-late scenarios . The socioeconomic assumptions are based on the 2023 scenarios released by the NGFS. Environmental assumptions refer to SSPs and RCPs from IPCC’s AR6. The analysis covers both transition and physical risks.

- Transition risk: Primarily evaluates impact of carbon pricing on corporate revenue, assuming that all domestic corporations must pay carbon fee, and estimating possible loss of revenue.

- Physical risk: Assess the impact of extreme weather events on corporate finances and operations, including downtime losses due to heavy rainfall, repair costs from asset damage caused by flooding and landslides, additional water expenses resulting from drought, and the effects of heatwaves on productivity and corporate income .

Long-term Scenario Analysis Outcome

Under the three climate transition scenarios—Orderly, Disorderly, and Too-little-too-late scenarios —the SCSB’s expected loss amounts for general corporate clients by 2050 account for 4.59%, 5.16%, and 6.52% of the baseline year (2024) net worth, respectively.

For individual clients, the expected loss amounts under the same scenarios represent 0.166%, 0.175%, and 0.194% of the baseline year net worth.

Among the three scenarios, the Too-little-too-late scenarios for 2050 is expected to result in the highest expected loss, with the combined expected loss for general corporate and individual clients accounting for 6.71% of the baseline year net worth.

Note 1: Pre-tax income (NT$15,010 million) refers to the SCSB’s pre-tax profit for the fiscal year 2024, as reporteded in the Q4 2024 financial statements.

Note 2: Net worth (NT$189,178 million) s the net worth after earnings distribution approved at the most recent shareholders' meeting for the past year.

Note 3: As the estimated expected losses under each scenario involve inherent uncertainty and do not represent the actual impacts that will occur in the future, caution should be exercised regarding the limitations when using and interpreting the analysis results.

Before implementing any management measures, the estimated financial impact of risks driven by changes in regulation was assessed based on the results of scenario analysis. Under the "Too-little-too-late scenario" in 2030, if corporate clients are required to pay carbon fees due to regulatory changes, the SCSB’s investment and financing profit may decline by approximately 56.715% of the profit before income tax in the baseline year. Based on the baseline year profit before income tax (NTD 15,010 million), the estimated financial impact would amount to NTD 8,512,921,500.

Short-term scenario

In a short-term scenario, it is assumed that the climate impact incident does not affect macroeconomy. The scenarios adopted include carbon fee scenario, intensity adjustment scenario. The analyzed risk types are as follows:

- Transition risk: The analysis adopts a carbon fee scenario aligned with the long-term pathway, focusing on evaluating the short-term impact of carbon pricing on the company.

- Physical risk: Based on a projected atmospheric environment with a 2°C increase in global temperature, the assessment estimates potential losses from work stoppages and asset impairment if a typhoon occurs within the next year.

Adjusted Intensity Scenario: Using Typhoon Morakot as a reference, rainfall statistics are adjusted based on climate change scenarios to assess the risk impact of typhoons.

Short-term Scenario Analysis Outcome

Under the short-term scenarios—Intensity adjustment, Transition risk, and Comprehensive Loss—the SC SB’s expected loss amounts for general corporate clients by 2050 account for 2.63%, 1.69%, and 2.64% of the baseline year (2024) net worth, respectively. For individual clients, the expected loss amounts under the same scenarios represent 0.159%, 0.163%, and 0.159% of the baseline year net worth. Among the three short-term scenarios, the Comprehensive Loss Scenario for 2050 is expected to result in the highest expected loss, with the combined expected loss for general corporate and individual clients accounting for 2.80% of the baseline year net worth.

Note 1: Pre-tax income (NT$15,010 million) refers to the SCSB’s pre-tax profit for the fiscal year 2024, as reporteded in the Q4 2024 financial statements.

Note 2: Net worth (NT$189,178 million) s the net worth after earnings distribution approved at the most recent shareholders' meeting for the past year.

To mitigate the impact of transition risks, the SCSB has formulated a decarbonization strategy for its investment and financing assets, aiming to reduce the carbon exposure of its portfolio. The strategy includes incorporating ESG risk assessments—covering environmental and nature-related factors—into the due diligence process. To implement the strategy, around 30 frontline employees have been assigned to perform risk assessments. Based on an average annual salary of NT$1,450,000 per non-managerial employee in 2024, the estimated cost of these management measures is NT$43,500,000.

Nature-related Dependencies and Impact Analysis

In 2024, IPBES, a biodiversity and ecosystem service intergovernmental science policy platform, released the Thematic Assessment Report on the Interlinkages among Biodiversity, Water, Food and Health. The report indicates that if global biodiversity continues to decline, it will lead to reduced food supply, water scarcity, weakened climate resilience, and a significant loss of natural capital, which will have a profound impact on the global economy.

As a financial institution, the SCSB not only plays a pivotal role in fostering industrial and economic development but also finds itself at the forefront of the impact amid the dynamic market environment. To ensure financial stability and fulfill its responsibility of promoting sustainable industrial development, in 2023, the SCSB adopted the Taskforce on Nature-related Financial Disclosures (TNFD) framework for the first time to initiate nature-related risk assessments. In 2024, the SCSB further deepened the assessment process, expanded the mapping of ecologically sensitive areas, and identified material nature-related risks and opportunities. The SCSB aims to strengthen nature-related risk controls and conduct due diligence for clients in highly ecologically sensitive areas. The SCSB seeks to enable its value chain partners to achieve the sustainable co-existence of environment, nature, and economy.

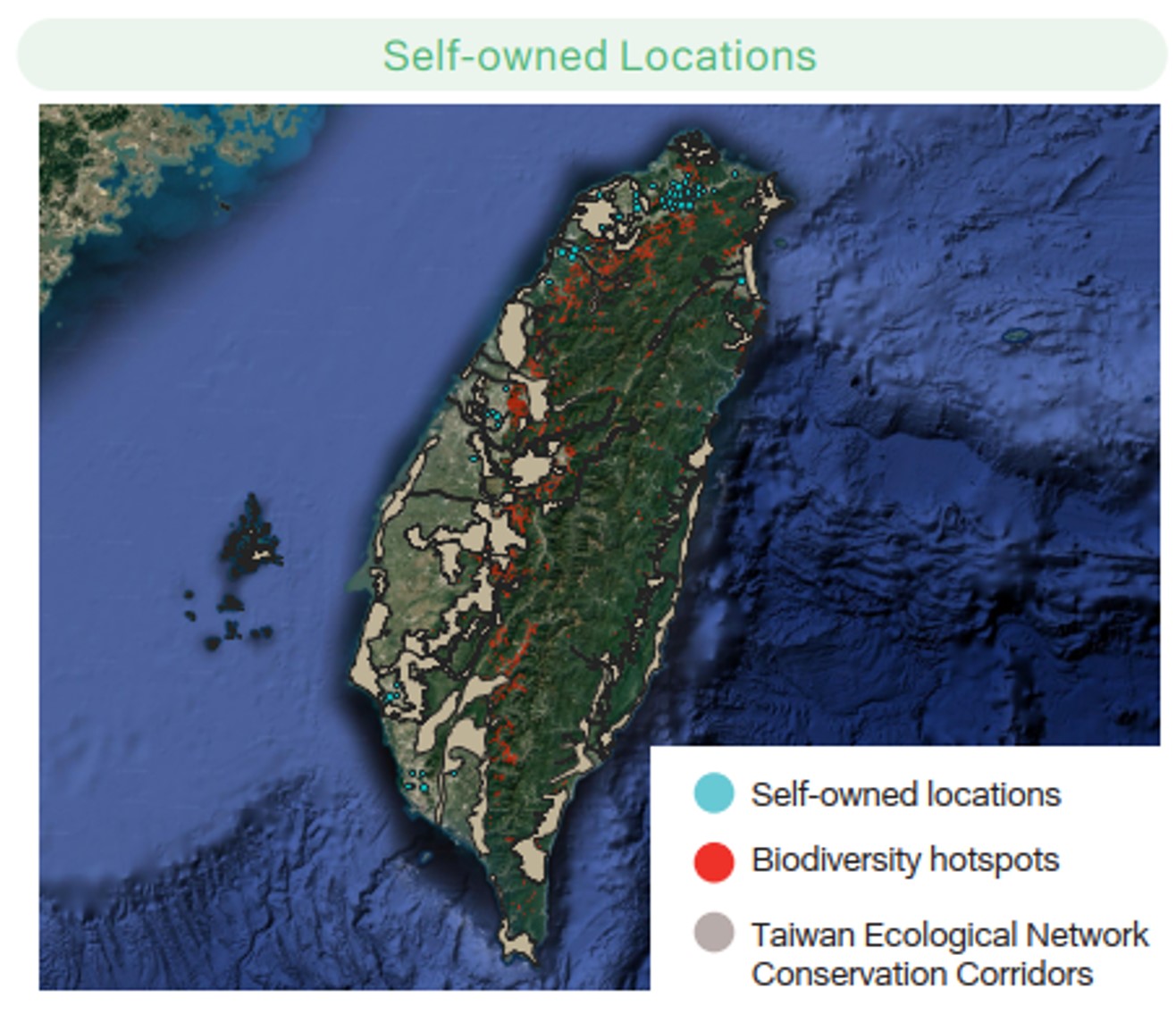

Spatial Assessment of Value Chain Intersections with Natural Ecosystems

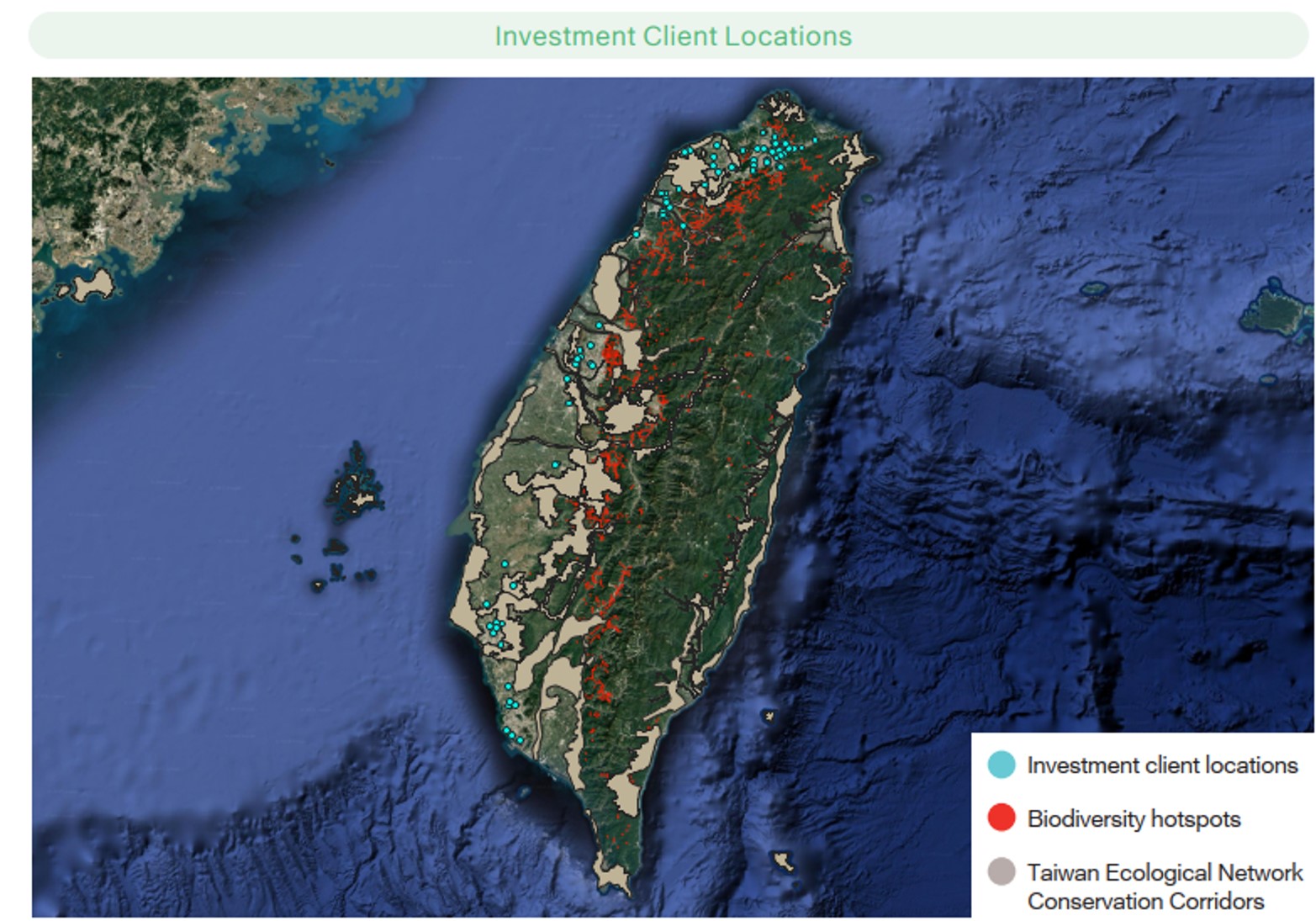

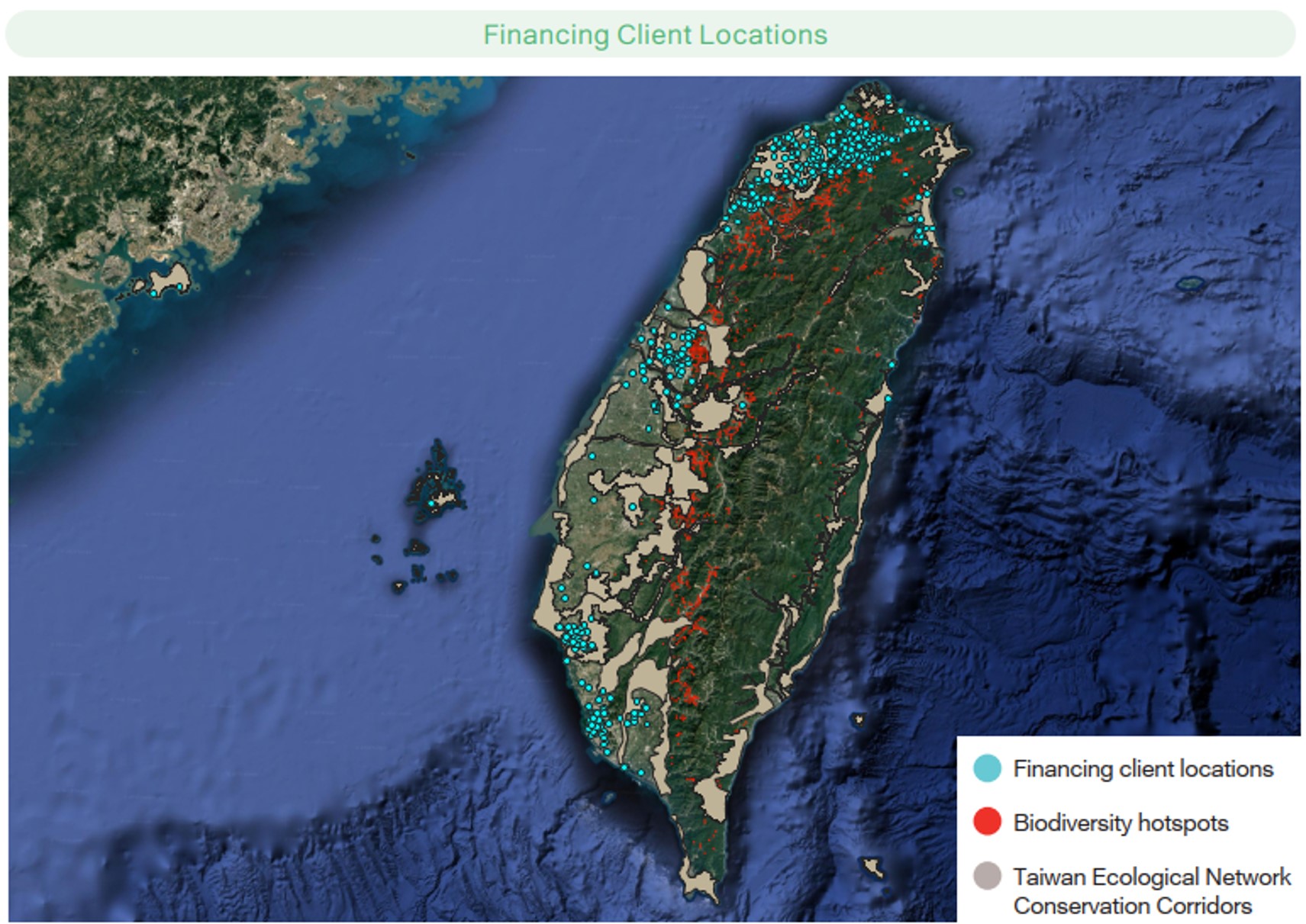

For all self-owned locations, supplier locations, and investment and financing clients in Taiwan, the SCSB utilized the “National Ecological Network Map” released by the Forestry and Nature Conservation Agency, Ministry of Agriculture, to analyze “Biodiversity Hotspots” based on overlay and estimation of the distribution data of 42 mammal species, 110 bird species, 25 amphibian species, 48 reptile species, and 82 insect species in Taiwan. Each hotspot is defined by a 1×1 km grid, and the diversity of various biological populations within the hotspot area ranks in the top 5% of Taiwan.

To further understand the value chain’s impact on the natural environment, in 2024, the SCSB expanded the scope to include regional conservation corridors in its analysis. The dataset includes 45 regional conservation corridors, including hills, rivers, plains, coasts, and offshore islands. These are fragmented ecosystems and priority conservation sites in all domestic upstream, midstream, and downstream areas.

To gain a complete understanding of the distance between the SCSB’s value chain activities and biodiversity hotspots and regional conservation corridors, the SCSB assessed whether its self-owned locations, supplier locations, and investment and financing clients were located within a 1,000-meter radius of biodiversity hotspots and regional conservation corridors. The analysis outcome is shown below:

Analysis of Self-owned and Supplier Locations

There were 74 self-owned locations. It is identified that none of these locations were situated near or within biodiversity hotspots. Seven self-owned locations were identified near or within regional conservation corridors: Nankan Branch, Guanyin Branch and Yangmei Branch in Taoyuan, North Hsinchu Branch in Hsinchu County, Tali Branch in Taichung, Nanke Branch in Tainan, and Pingtung Branch in Pingtung County.

There were 198 supplier locations. It is identified that four of them were situated near or within biodiversity hotspots, Neihu District in Taipei and Ruifang District, Xindian District and Shenkeng District in New Taipei City. There were 7 supplier locations situated near or within regional conservation corridors, Tamshui District in New Taipei City, Luzhu District, Bade District and Yangmei District in Taoyuan, Zhubei City in Hsinchu County, Pingtung City in Pingtung County, and Hualien City in Hualien County.

There were 169 investment client locations. It is identified that none of these locations were situated near or within biodiversity hotspots. There were 20 of them situated near or within regional conservation corridors of the ecological network. These regional conservation corridors include the Wetland Conservation Corridor of Taoyuan Pond Plain in Taoyuan, the Conservation Corridor of Fengshan River and Touqian River Basin, the Qianshan Conservation Corridor of Dadu Terrace in Taichung, and the Grass-covered Land Conservation Corridor of Southern Chia Nan Plain in Tainan and Chiayi.

There were 838 financing client locations. It is identified that 21 of these locations were situated near or within biodiversity hotspots. There were 154 of them situated near or within regional conservation corridors of the ecological network. These overlapping areas are mainly concentrated in Taiwan’s six major municipalities and other regions with high industrial and commercial activity. The SCSB will continue to enhance monitoring and management of such clients to mitigate potential risks associated with natural environmental impacts.

Natural Risk Management Performance

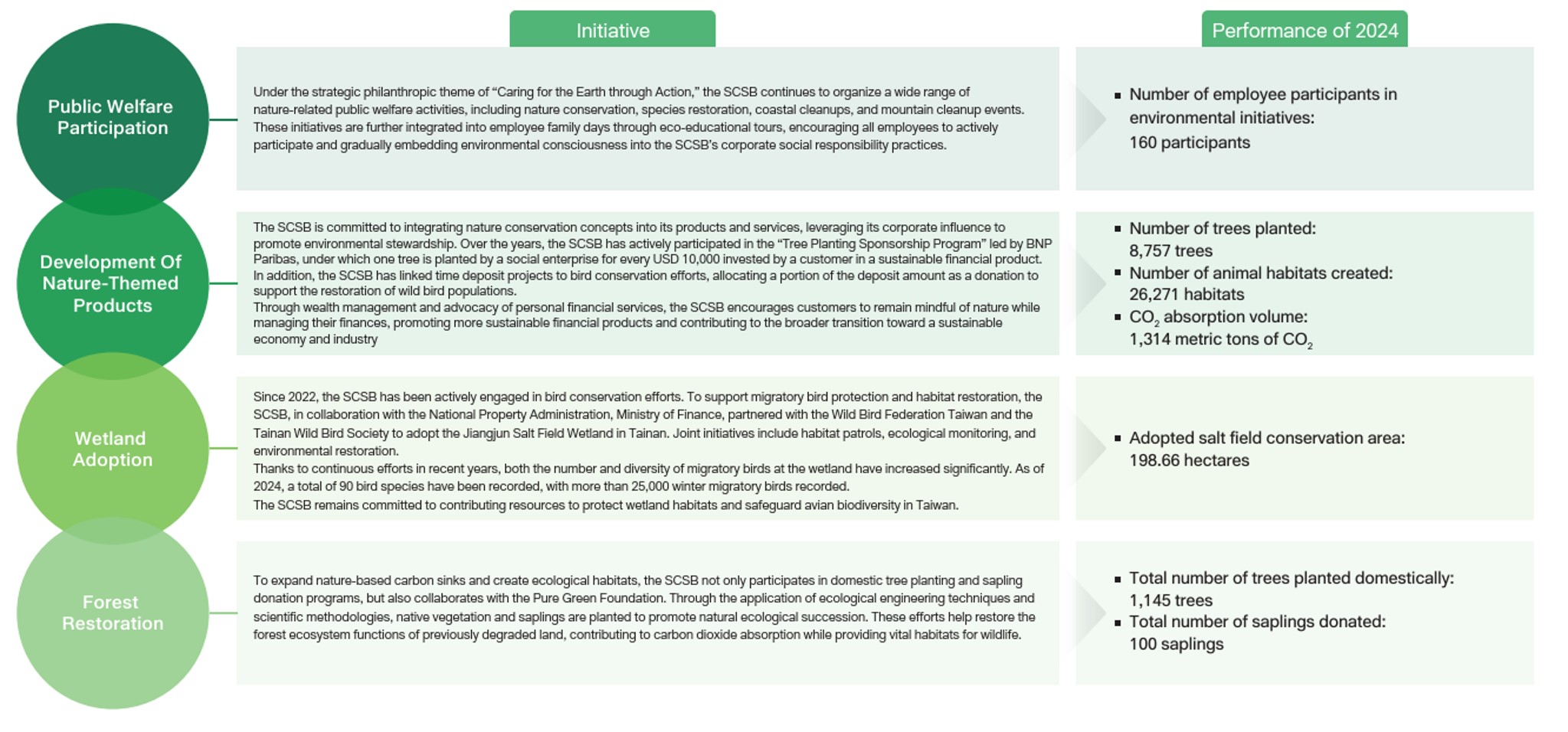

To strengthen the management of natural related impacts, the SCSB has implemented relevant measures across various segments of its value chain to reduce environmental burdens and preserve ecosystem integrity. In recent years, the SCSB has actively advanced natural related initiatives such as “public welfare participation”, “development of nature-themed products”, “wetland adoption”, and “forest restoration” aiming to contribute to ecological restoration and promote environmental sustainability with a diverse range of actions.

The performance of these nature-focused initiatives in 2024 is summarized as follows:

Indicator and target

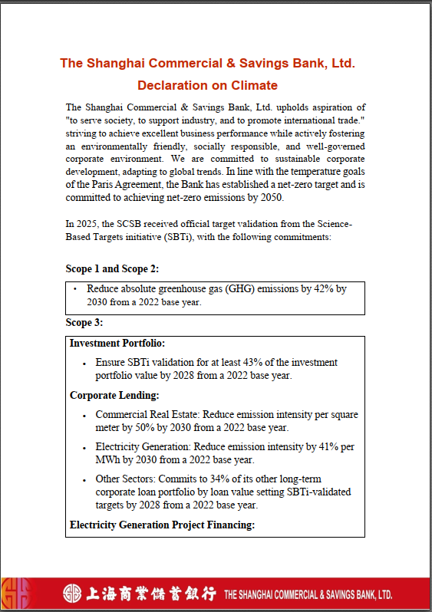

The SCSB fully checks the GHG emissions of all operating locations to show its firm commitment to sustainable operation and net zero transitions. The SCSB integrates carbon emissions data of investment and financing clients, and sets a carbon emission reduction goal that meets the Paris Agreement. At the end of 2024, the SCSB officially submitted target verification application to the Science Based Targets Initiative (SBTi) and passed approval at the beginning of 2025. To realize the carbon reduction pathway, the SCSB has drawn up the carbon reduction plan covering overseas subsidiaries, showing commitment to sustainable development, and continues with carbon reduction steadily..

Note1: The greenhouse gases covered by the SBT targets include: CO₂, CH₄, N₂O, HFCs, PFCs, SF₆, and NF₃.

Note2:In the baseline year (2022), Scope 1 greenhouse gas emissions from the SCSB and all subsidiaries within the financial reporting boundary totaled 1,029.719 metric tons, and Scope 2 emissions were 11,686.174 metric tons, resulting in a combined total of 12,715.893 metric tons.

The SCSB has introduced the GHG inventory system and the ISO management system associated with environment, energy, and water resources to ensure that the carbon reduction information of all operating locations and the Head Office is consistent. The SCSB also keeps the management process standardized to take carbon reduction actions effectively. In the short run, our primary reduction strategy is equipment replacement. By introducing highly efficient energy-saving equipment and replacing conventional fuel cars with hybrids or electric cars, carbon emissions during operation are reduced. In the long run, the SCSB will continue to track and optimize the carbon reduction measures by fulfilling the energy resource management target. Meanwhile, the SCSB gradually increases the ratio of renewable energy purchase and carbon offset to effectively fulfill the carbon reduction commitment in the short, medium and long run.

Note 1: The definition of other industries in the SCSB covers the petrochemical industry, steel industry, paper industry, concrete industry, transportation service industry, electronic manufacturing industry, financial industry, retail industry, dining and accommodation industry, and real estate development industry.

Note 2: The target boundary covers all companies included in the SCSB’s consolidated financial statements.

Note 3: The greenhouse gases covered by the SBT targets include: CO₂, CH₄, N₂O, HFCs, PFCs, SF₆, and NF₃.

Full target:https://files.sciencebasedtargets.org/production/files/Target-language-and-summary-The-SCSB.pdf

Environmental and Energy Management Mechanism

The SCSB has implemented ISO 14001-Environmental Management System, ISO 50001-Energy Management System, and ISO 46001-Water Efficiency Management System. Moreover, the SCSB formulated an "Environmental, Occupational Safety and Health, Energy and Resource Management Policy" to promote various voluntary actions and improvement plans. Through systematic management approaches, achieve to reduce energy and water consumption and minimize waste generation, fulfilling our responsibility towards environmental friendliness.

The SCSB regularly collects and studies the law as well as the opinions of internal and external stakeholders to identify environmental and energy-related risks and opportunities that may have a significant impact on the SCSB by following the PDCA cycle, as well as to continue improving environmental and energy performance.

Since the SCSB is in the financial services sector, our main environmental impact during internal operations is resource consumption, particularly paper usage. To address this problem, the SCSB has implemented policies such as promoting electronic forms, paperless meetings, as well as paper recycling and classification to minimize paper consumption. In terms of direct and indirect energy and resource consumption, the SCSB consumes mainly water, electricity, and fuel for official vehicles. To mitigate its environmental impact, the SCSB has implemented policies such as procuring energyefficient equipment, optimizing lighting intensity, installing timers for lighting control, managing air conditioning usage, adjusting water flow, and performing regular maintenance and management of official vehicles. In compliance with relevant environmental regulations, the SCSB is committed to protecting the natural environment by enhancing the efficiency of resource utilization in its operational activities and internal management practices.

Energy Management

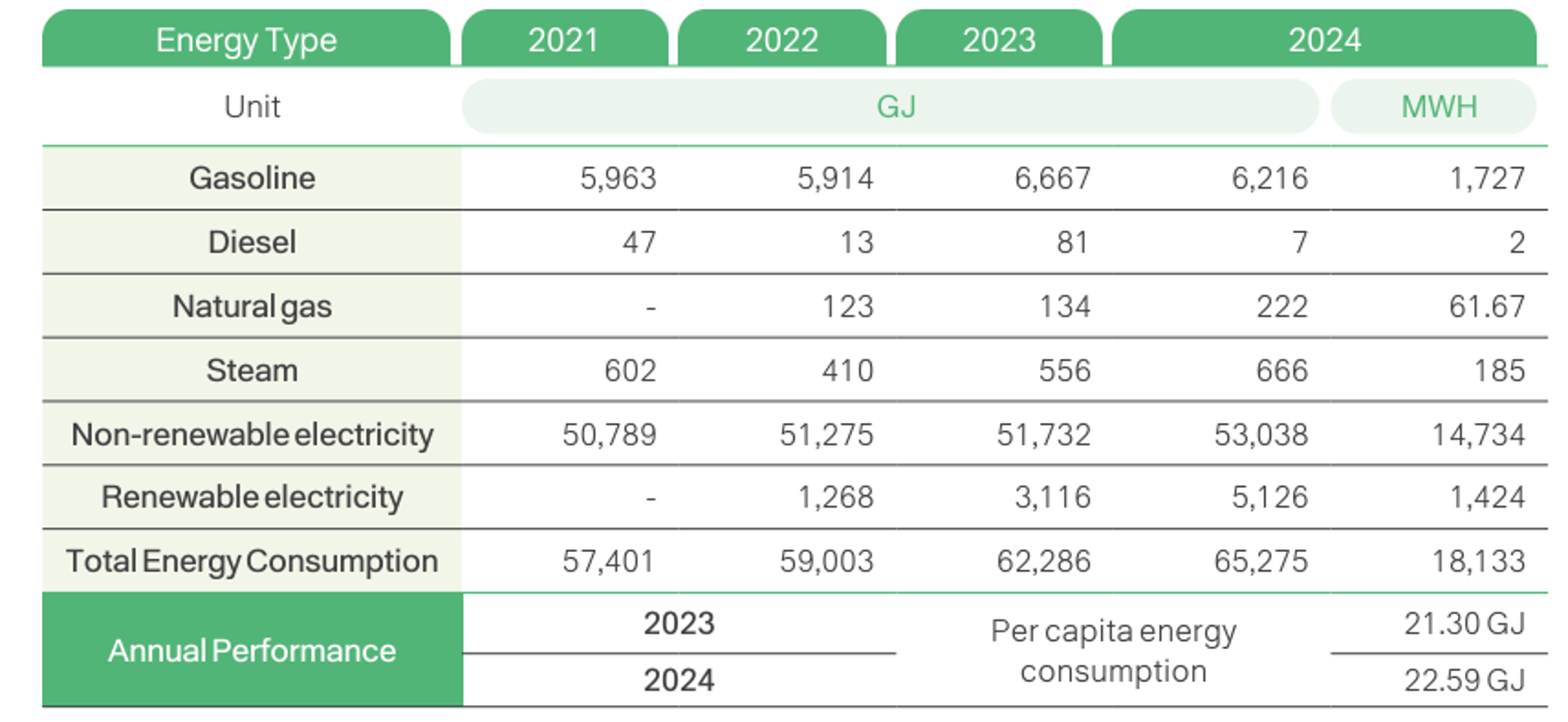

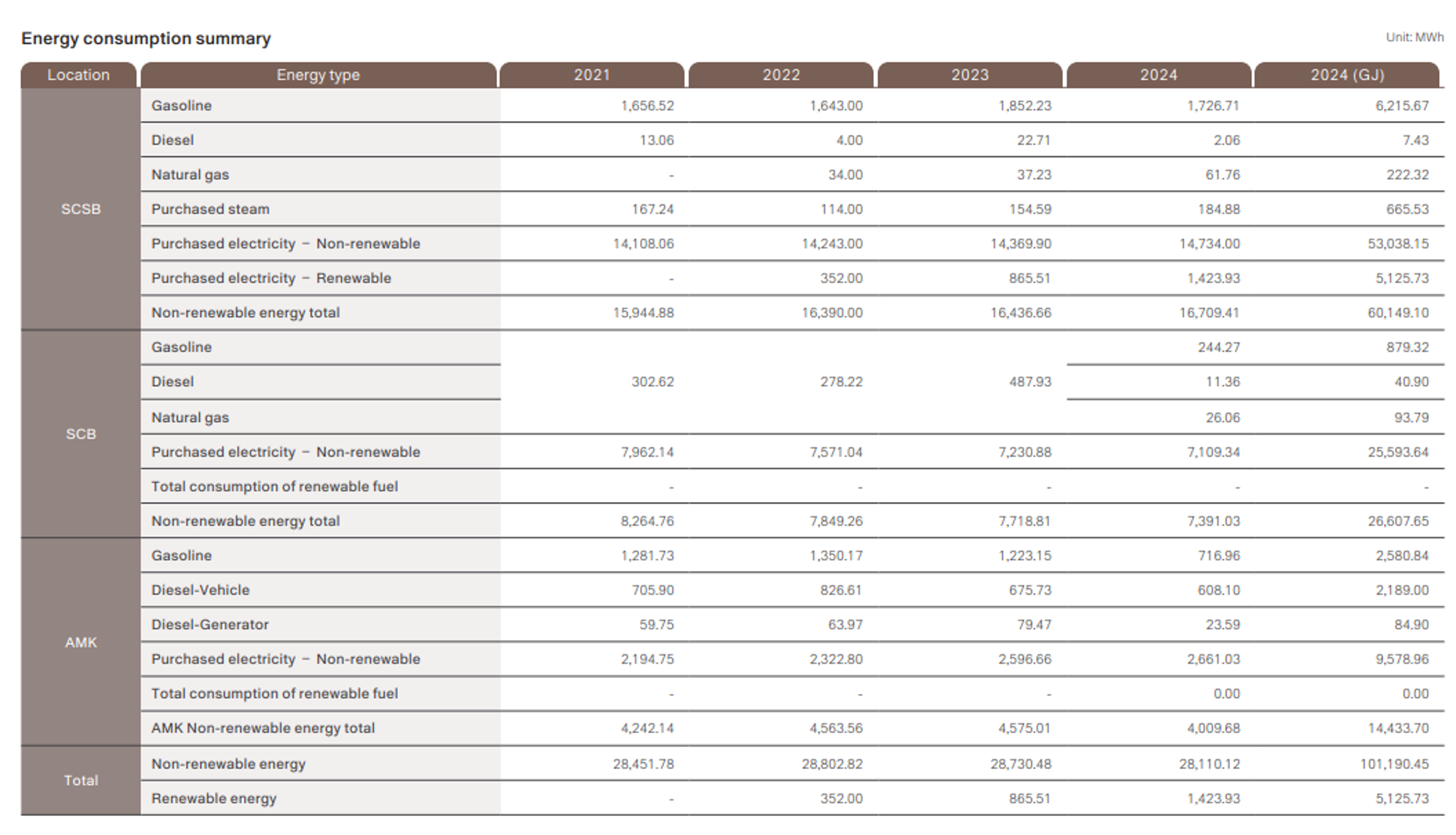

The energy consumption of each the SCSB operating location mainly consists of electricity and gasoline fuel for official vehicles. In 2024, the total energy consumption of the SCSB was 65,275 GJ, which is a 4.8% increase from last year's 62,286 GJ. Per capita energy consumption was 22.59GJ, up by 6.06% from 21.30 GJ last year.

Note 1:The target for 2024 is to reduce per capita energy consumption by 3% compared to the previous year.

Note 2:Energy unit conversion is calculated based on 1 cal=4.184 J, 1GJ=0.2778 MWh.

Note 3:The calorific values of automotive gasoline, diesel, and natural gas in Taiwan are calculated based on the "Unit Calorific Value Table of Energy Products" published by the Energy Administration of the Ministry of Economic Affairs. The coefficients are 7,800 kcal/l, 8,400 kcal/l, and 9,000 kcal/m3 respectively.

Note 4:Automotive gasoline in Vietnam, Indonesia, and Thailand is based on Greenhouse gas reporting: conversion factors 2024、《Indonesia: Fuels: Diesel And Gasoline》,and 《The Comparison of Fuel Consumption for Small Gasoline Engine Fuelled by Commercial Gasoline Fuel in Thailand on Different Conditions》. The calorific value coefficients are 33.61 MJ/L、33.264 MJ/L、31.48 MJ/L respectively.

Note 5:Automotive gasoline in China is calculated according to the National Standard for Automotive Gasoline GB 17930-2016, with a density ranging from 720 to 775 kg/m³, averaging 747.5 kg/m³. Calculations are based on the General Principles for Calculation of Total Energy Consumption GB/T 2589-2020, which provides a calorific value of 10,300 kcal/kg, resulting in a final calorific value coefficient of 7,699 kcal/L; purchased steam is calculated based on the calorific value announced in the "General Principles for Calculation of Total Energy Consumption GB/T2589-2008," with a calorific value coefficient of 3.763 GJ/ton; natural gas is calculated based on the calorific value announced in "General Principles for Comprehensive EnergyConsumption Calculation GB/T2589-2020", and the calorific value coefficient is 0.0356 GJ/ cubic meters.

Note 6:Natural gas used in Hong Kong is based on the Towngas bill calorific value of 48 megajoules (MJ) per KWh, while natural gas used in Singapore is based on the City Energy Handbook on Gas Supply calorific value of 38.3 MJ/m³.

Note 7:The calorific value coefficient for purchased electricity in overseas and Taiwan regions is 3,600 GJ per million KWh.

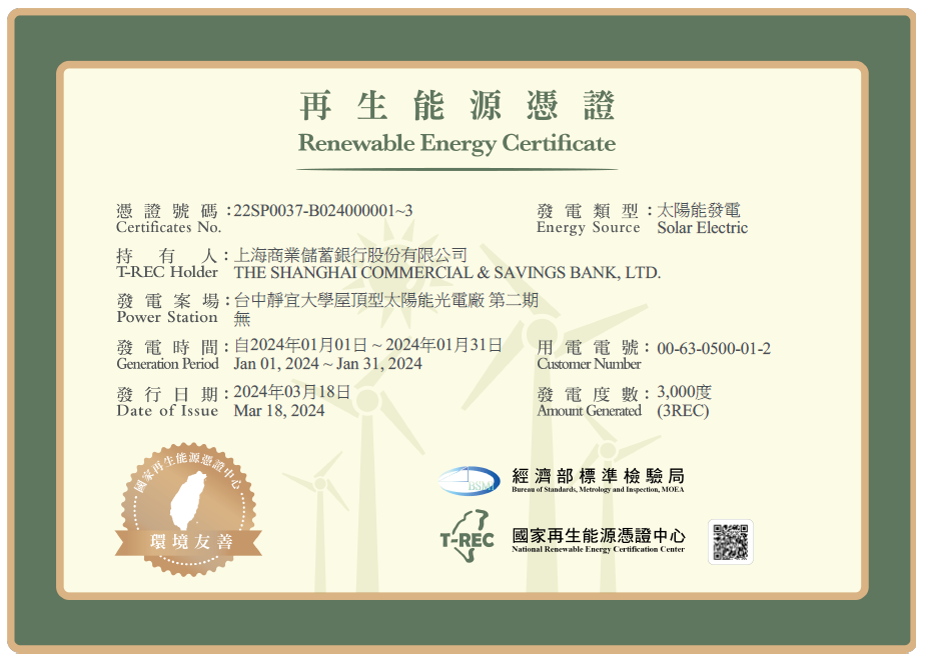

Note 8:Renewable electricity is purchased directly. A total of 1,420 certificates were purchased in 2024, totaling 1,423,815 kWh.

Note 9:The data statistics includes the Shanghai Commercial and Savings Bank's operating sites in Taiwan, overseas branches, and overseas representative offices (91 locations in total).

Water Resources Management

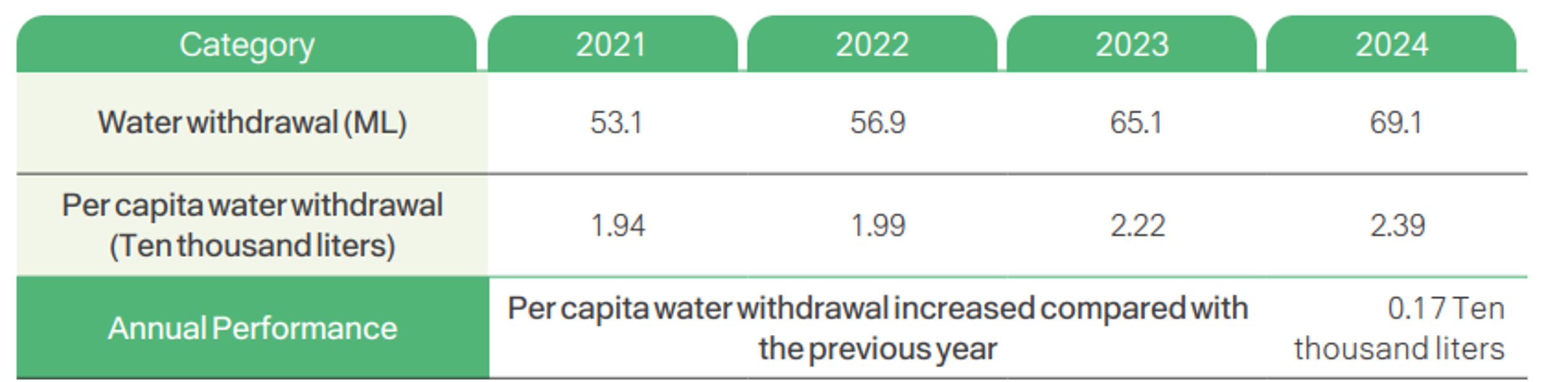

Water was provided to office buildings and service locations for employees and some clients, without directly impacting water sources. Wastewater was discharged into the sewage system, collected through a network of pipelines, and sent to sewage treatment plants, thereby preventing pollution of other surface water bodies. Furthermore, the SCSB has implemented water-saving measures for toilet water usage and other water-consuming equipment and purchased products with watersaving certification marks. To enhance water management, we have implemented the ISO 46001 Water Efficiency Management System. Through the analysis of water usage activities, we identify facility areas with water-saving potential and make adjustments to water output accordingly. In 2024, the SCSB´s total water withdrawal was 69.1 ML, an increase of 4.0 ML compared to 65.1 ML in 2023. The water withdrawal per capita was 2.39 ten thousand liters, an increase of 0.17 ten thousand liters from the previous year, representing a growth rate of approximately 7.6%. The main reason for the increase in water withdrawal was the addition of an employee cafeteria in the new headquarters building.

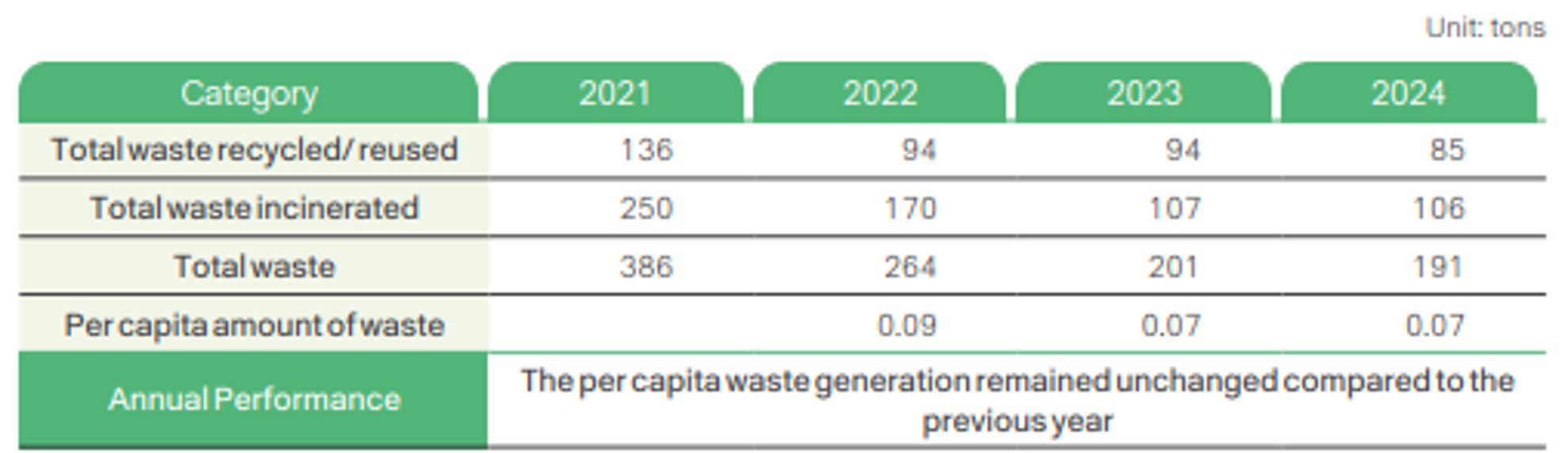

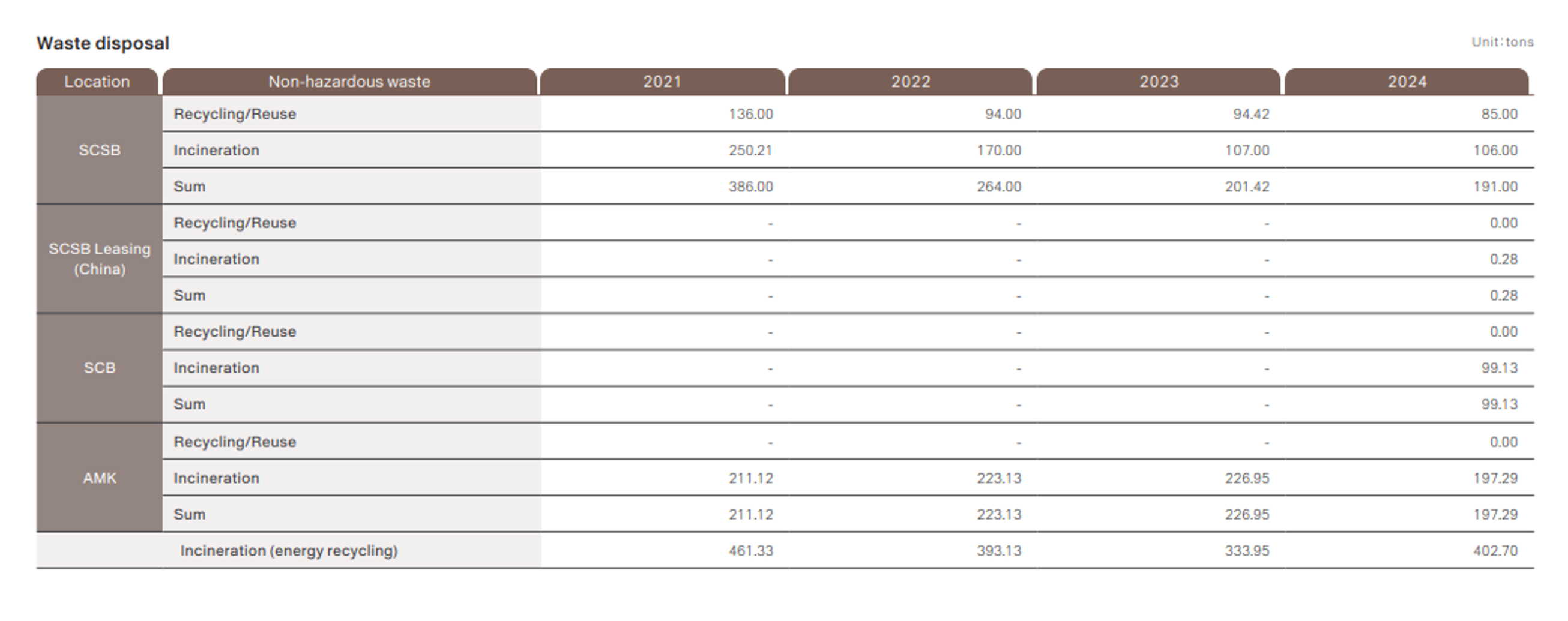

Note 1:The target for 2024 is to reduce the amount of non-recyclable waste per capita by 3% from the previous year.

Note 2:Reuse methods for non-hazardous waste include only recycling/reuse and incineration. It does not include reuse, composting, recycling, deep well injection, burial, on-site storage, etc.

Note 3:The data statistics includes the Shanghai Commercial and Savings Bank's operating sites in Taiwan, overseas branches, and overseas representative offices (91 locations in total).

Waste Management

The SCSB operates in the financial services sector and generates only non-hazardous waste. The SCSB encouraged employees to practice waste classification. Currently, designated recycling areas have been created in the headquarters building and branches to perform waste classification. Entrust legal recycling companies to dispose of waste by recycling, incineration, or landfill. Therefore, waste generated during the SCSB's operations did not lead to serious environmental pollution. In 2024, 191 tons of waste was generated across all branches, reflecting a decrease of 10 tons compared to 2023. Nonrecyclable waste was 106 tons. Overall, the per capita amount of non-recyclable waste in 2024 was approximately 0.07 tons.

Note 1:The target for 2024 is to reduce the amount of non-recyclable waste per capita by 3% from the previous year.

Note 2:Reuse methods for non-hazardous waste include only recycling/reuse and incineration. It does not include reuse, composting, recycling, deep well injection, burial, on-site storage, etc.

Note 3:The data statistics includes the Shanghai Commercial and Savings Bank's operating sites in Taiwan, overseas branches, and overseas representative offices (91 locations in total).

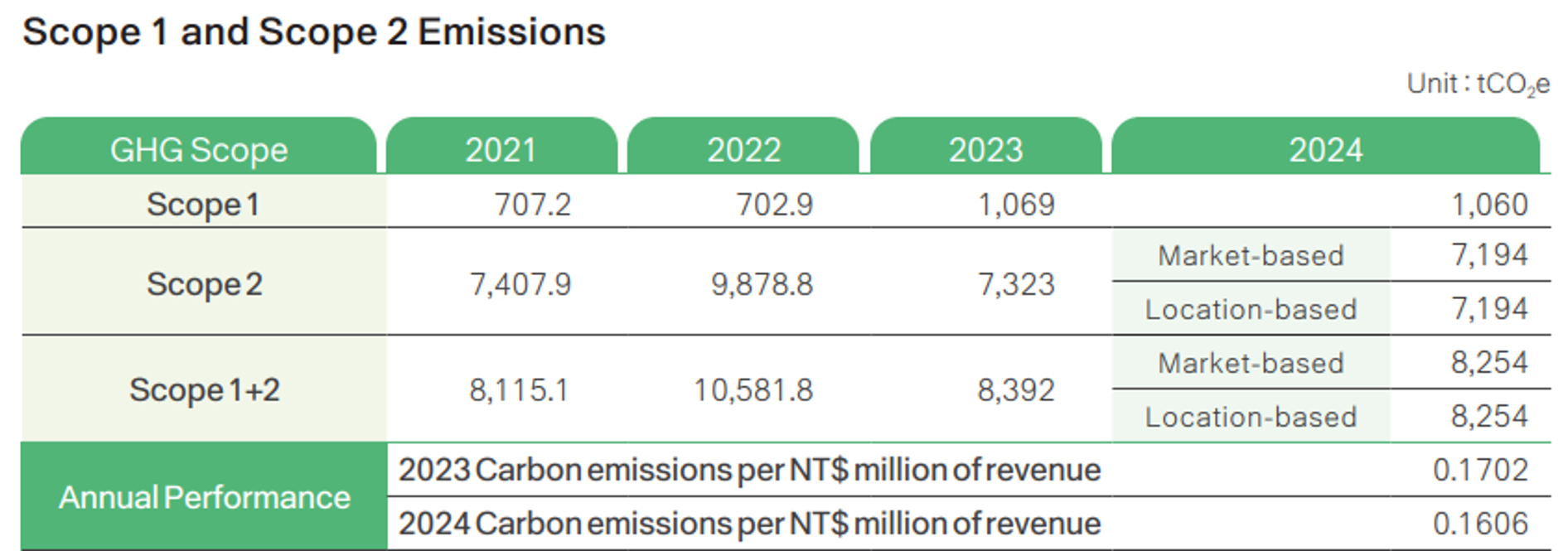

Greenhouse Gas Emission Management

The SCSB conducted a GHG inventory following ISO 14064-1:2018 Greenhouse Gases Part 1. The organizational boundaries were set using the operation control method and emissions were calculated by applying the emission factor method. The coefficients were derived from the GHG Inventory Table 6.0.4 published by the Ministry of Environment and the electricity emission coefficients published by the Energy Administration.

To achieve sustainable operations and implement carbon reduction measures, the SCSB has set a target to reduce absolute emissions by 42% by 2030, from the base year of 2022.The Scope 1 emissions for 2024 were similar to those in 2023, while Scope 2 emissions decreased by 1.8% compared to 2023. The combined Scope 1 and Scope 2 emissions per million revenue in 2024 were 0.1606 tCO2e, reflecting a decrease of 5.64% compared to last year, thereby achieving the goal of reducing carbon emissions per NT$ million of revenue by 3% compared to last year.

Note 1:The target to be achieved in 2024 is a 3% reduction in Scope 1 and Scope 2 carbon emissions per million of NT$ revenue compared to the previous year.

Note 2:The global warming potential (GWP) is based on the IPCC Sixth Assessment Report in 2021-2024.

Note 3:The electricity carbon emission coefficient in Taiwan adopts the 2024 electricity carbon emission coefficient announced by the Energy Administration of the Ministry of Economic Affairs. The coefficients in other regions adopt the local carbon emission coefficient or the data of each region in the Ecoinvent environmental database.

Note 4:The remaining emission coefficients other than electricity mainly refer to the "Greenhouse Gas Emission Coefficient Management Table Version 6.0.4" announced by the Ministry of Environment of the Executive Yuan. The GHG emission coefficient for steam is taken from the Ecoinvent environmental database.

Note 5:The greenhouse gas emissions inventory uses the "operation control" method and the statistical gas categories include CO2, CH4, N2O, HFCs, PFCs, SF6, and NF3.

Note 6:The SCSB’s Scope 1 and Scope 2 greenhouse gas (GHG) emissions for 2024 were verified by a third party and received an ISO 14064-1:2018 Greenhouse Gas Part 1 verification statement. The verification was conducted by SGS in May 2025, covering the period from January 1 to December 31, 2024. The scope of the verification includes all SCSB locations in Taiwan.

Note 7:The data statistics includes the Shanghai Commercial and Savings Bank's operating sites in Taiwan, overseas branches, and overseas representative offices (91 locations in total).

Note 8: The Scope 1 and Scope 2 greenhouse gas (GHG) emissions data of the SCSB for previous years (2021 to 2023) have been verified by SGS. The related verification statements have been published on the SCSB’s “Energy and resource management” webpage.

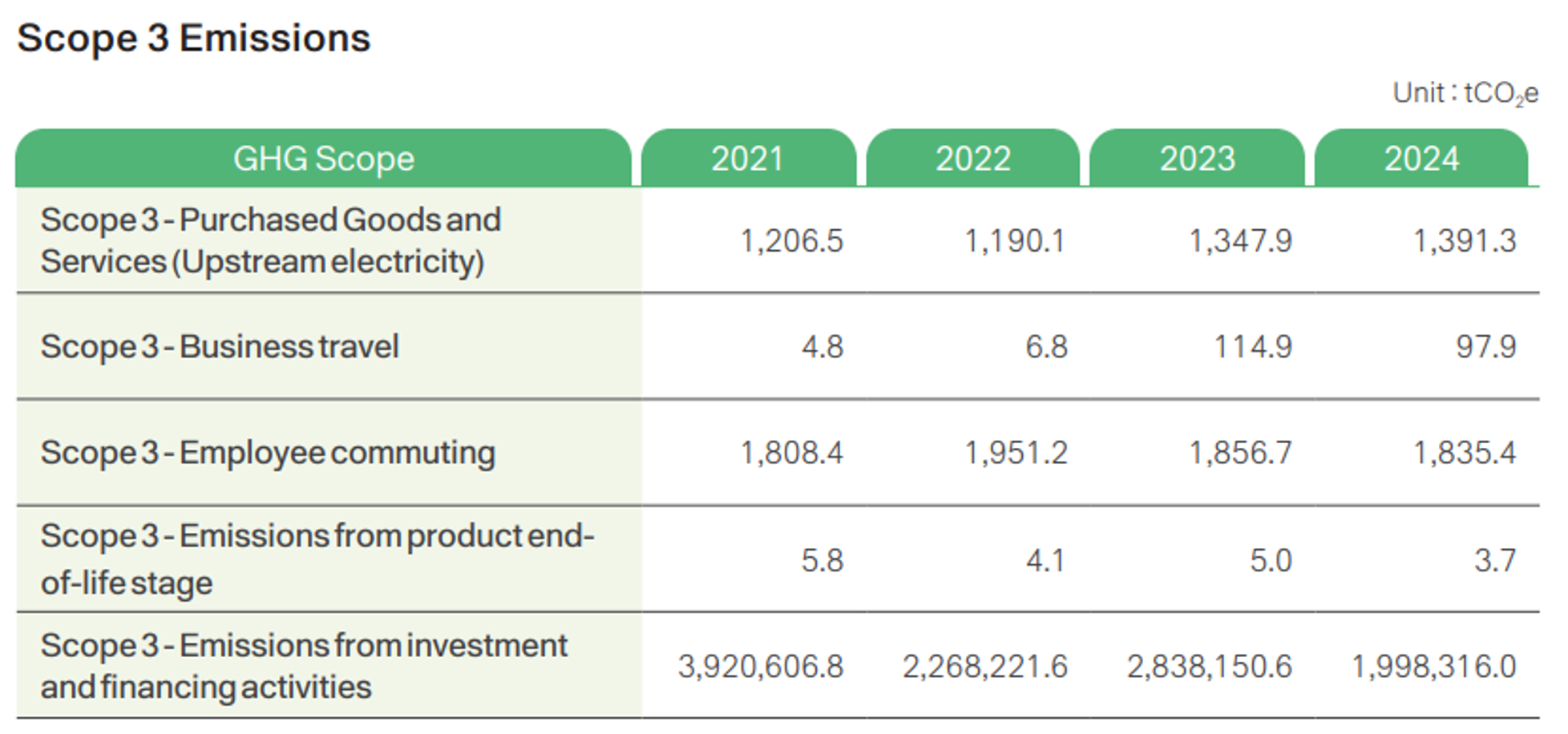

Note 1:The target to be achieved in 2024 is a 3% reduction in carbon emissions per NT$ million revenue compared to the previous year.

Note 2:The global warming potential (GWP) is taken from the IPCC Sixth Assessment Report 2021.

Note 3:The upstream electricity carbon emission coefficient adopts the Product Carbon Footprint Information Network-Electricity Indirect Carbon Footprint (2021).

Note 4:For the emission coefficients of employee commuting and business travel, domestically, the Product Carbon Footprint Information Network and the Ministry of the Environment's "Taiwan Vehicle Life Cycle Assessment" research project are adopted. Overseas, the coefficients for each region are taken from the Ecoinvent environmental database. The statistics of emission of employee commuting include both domestic and overseas employees.

Note 5:End-of-life emissions are based on the SCSB 2023 Credit Card Carbon Footprint Report (valid until 15 February 2028).

Note 6:Emissions from investment and financing activities are inventoried and calculated according to the PCAF methodology.

Note 7:The data statistics includes the The Shanghai Commercial and Savings Bank's headquarters, branches, and offices (91 locations in total)

Note 8:Excluding emissions from investment and financing activities, all Scope 3 GHG emissions data for the SCSB’s Taiwan operations in 2024 were independently verified by SGS in May 2025. The SCSB received a verification statement in accordance with ISO 14064-1:2018, covering the period from January 1 to December 31, 2024.

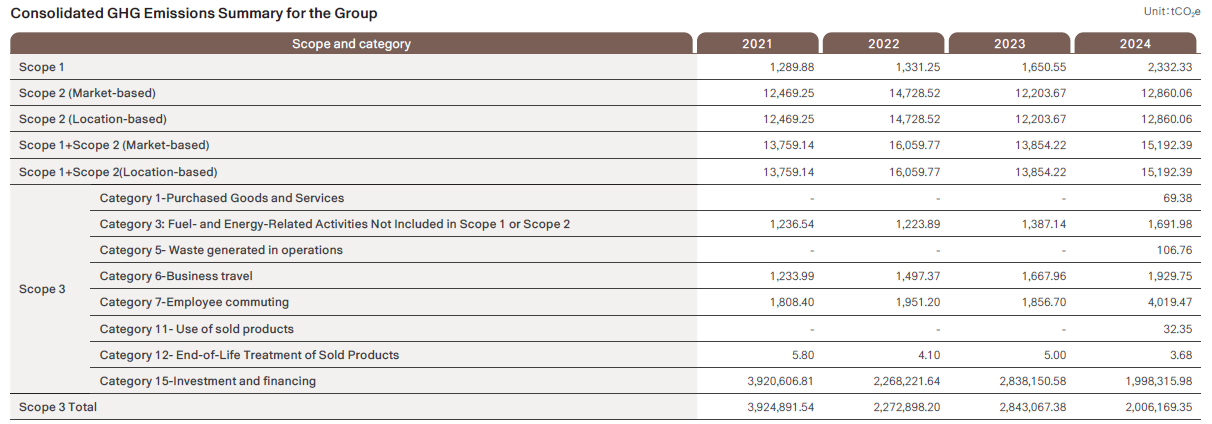

Environmental Data & Performance of the Group

Note 1: From 2021 to 2023, the GHG inventory boundary covered SCSB, SCB, SCSB Leasing (China), and AMK. In 2024, in response to SCSB’s SBT targets and to comprehensively account for emissions from subsidiaries, the inventory scope was expanded to include SCSB Asset Management Ltd., SCSB Marketing Ltd., and China Travel Service (Taiwan). Categories 1,5 and 11 were also added. Due to the expansion of both inventory boundaries and categories, emissions in each scope increased compared to previous years.

Note 2: In May 2025, the 2024 Scope 1 and Scope 2 GHG emissions data of SCSB and its subsidiaries, as well as Scope 3 emissions data (excluding investment and financing activities), were independently verified by SGS Taiwan Ltd. The SCSB obtained a verification statement in accordance with ISO 14064-1:2018, covering the period from January 1 to December 31, 2024.

The coverage rate of GHG emissions data in 2024 was calculated based on headcount, with the denominator representing the total number of group employees and the numerator representing the number of employees from entities whose GHG emissions data was collected: 8,779 / 8,779 = 100%.

The total group headcount includes employees from the SCSB, SCB, SCSB Leasing (China), AMK, SCSB Asset Management Ltd., SCSB Marketing Ltd., and China Travel Service (Taiwan).

The coverage rate of water resource data in 2024 was calculated based on headcount, with the denominator representing the total number of group employees and the numerator representing the number of employees from entities whose water resource was collected: 8,534 / 8,779 = 97.2

The total group headcount includes employees from the SCSB, SCB, SCSB Leasing (China), AMK, SCSB Asset Management Ltd., SCSB Marketing Ltd., and China Travel Service (Taiwan).

The coverage rate of energy data in 2024 was calculated based on headcount, with the denominator representing the total number of group employees and the numerator representing the number of employees from entities whose energy data was collected: 8,534 / 8,779 = 97.2%

The total group headcount includes employees from the SCSB, SCB, SCSB Leasing (China), AMK, SCSB Asset Management Ltd., SCSB Marketing Ltd., and China Travel Service (Taiwan).

The coverage rate of waste disposal data in 2024 was calculated based on headcount, with the denominator representing the total number of group employees and the numerator representing the number of employees from entities whose waste disposal data was collected: 8,549 / 8,779 = 97.4%

The total group headcount includes employees from the SCSB, SCB, SCSB Leasing (China), AMK, SCSB Asset Management Ltd., SCSB Marketing Ltd., and China Travel Service (Taiwan).

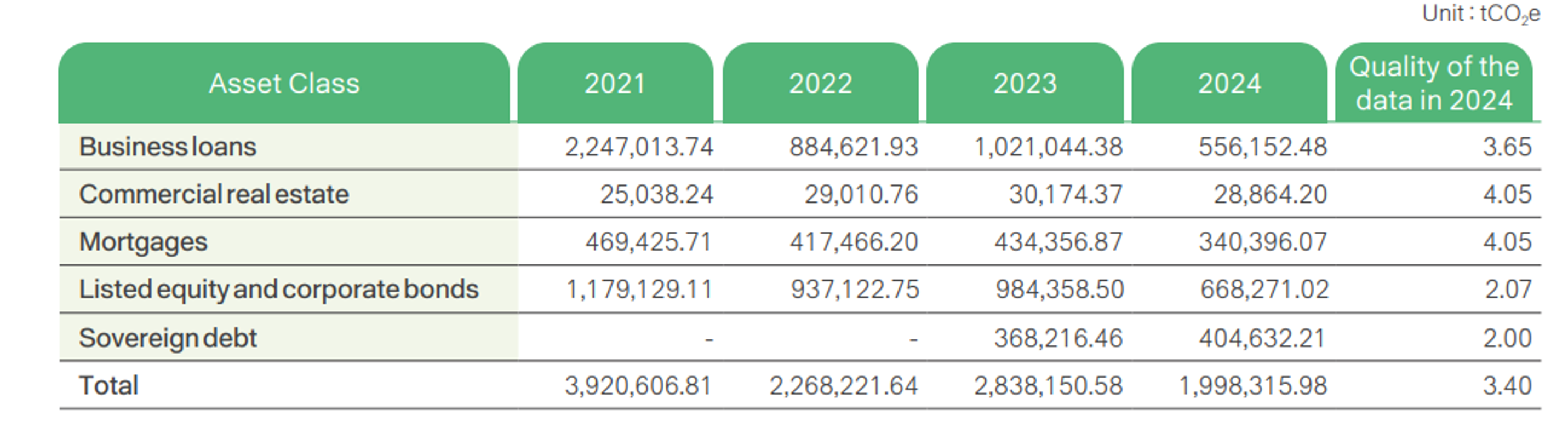

Scope 3 - Emissions from investment and financing activities

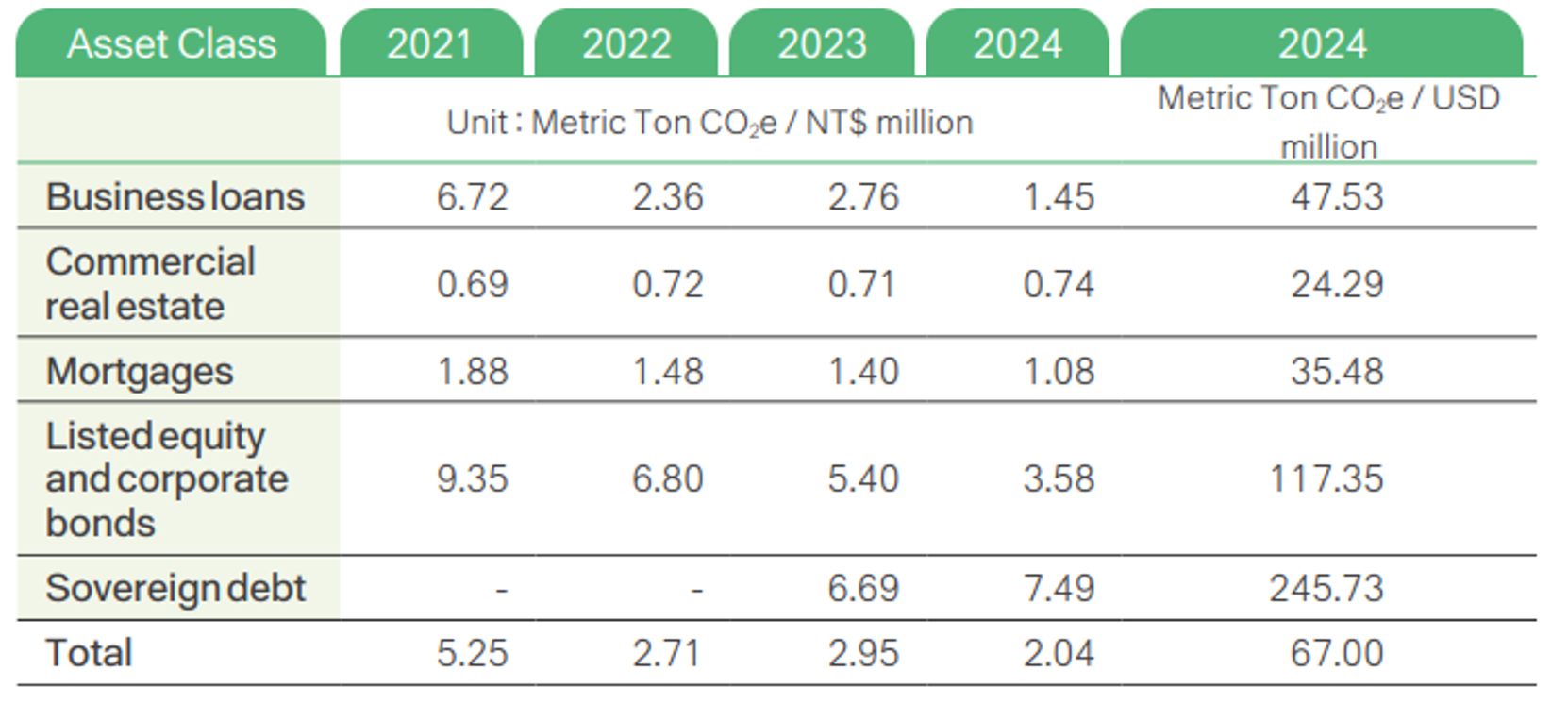

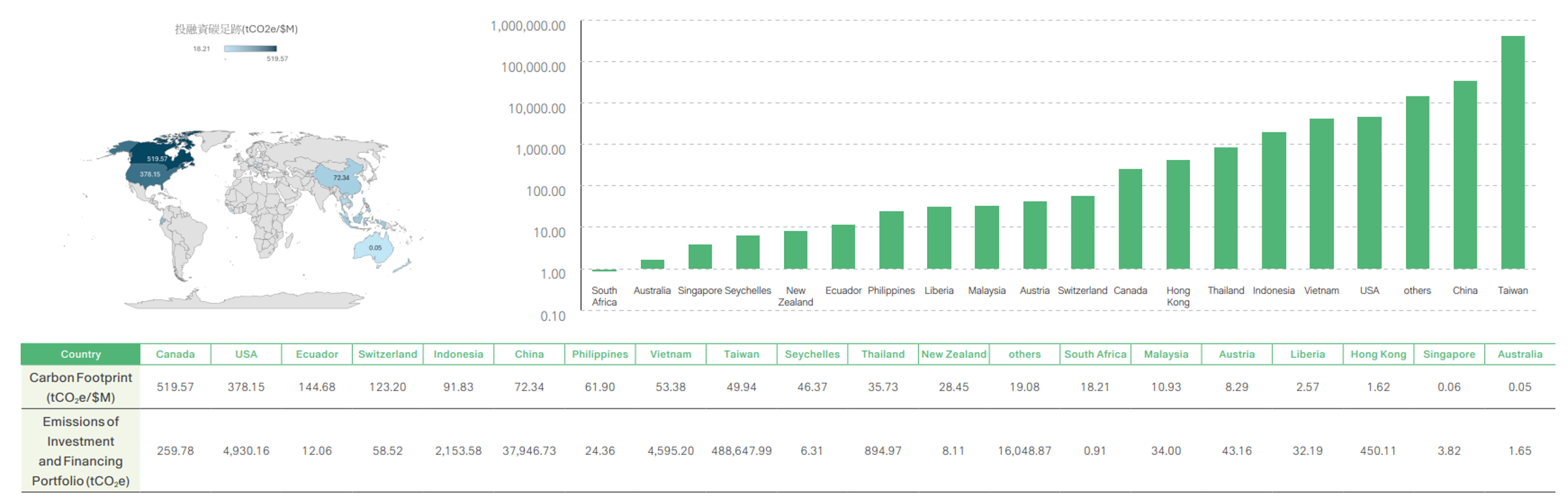

The SCSB calculates the carbon emissions of investment and financing portfolios in accordance with the Partnership for Carbon Accounting Financials (PCAF) methodology. The total carbon emissions of the investment and financing portfolio in 2024 amounted to 1,998,315.98 metric tons of CO2e . The carbon footprint of the investment and financing portfolio was 2.04 metric tons of CO2e / NT$ million (approximately 67.00 metric tons of CO2e / million USD). Most asset categories showed a declining trend in carbon footprint from 2021 to 2024. The SCSB will continue to monitor the carbon emissions of the investment and financing portfolio and assist investment and financing targets in transitioning to low-carbon operations through engagement.

Asset Class Comparison

GHG Emissions of Investment and Financing Portfolio(tCO2e)

Note 1:Business loans do not include commercial real estate, mortgages, and project financing.

Note 2:From 2021 to the end of 2024, the SCSB has no automobile and motorcycle mortgage loan positions.

Note 3:In 2024, the SCSB´s investment and financing emission coverage rate is 92.04% .(holdings included in calculation/total existing holdings)

Investment and Financing portfolio Carbon Footprint

Note 1:Business loans do not include commercial real estate, mortgages, and project financing.

Note 2:From 2021 to the end of 2024, the SCSB has no automobile and motorcycle mortgage loan positions.

Note 3:In 2024, the SCSB´s investment and financing emission coverage rate is 92.04%. (holdings included in calculation/total existing holdings)

Industry Comparison

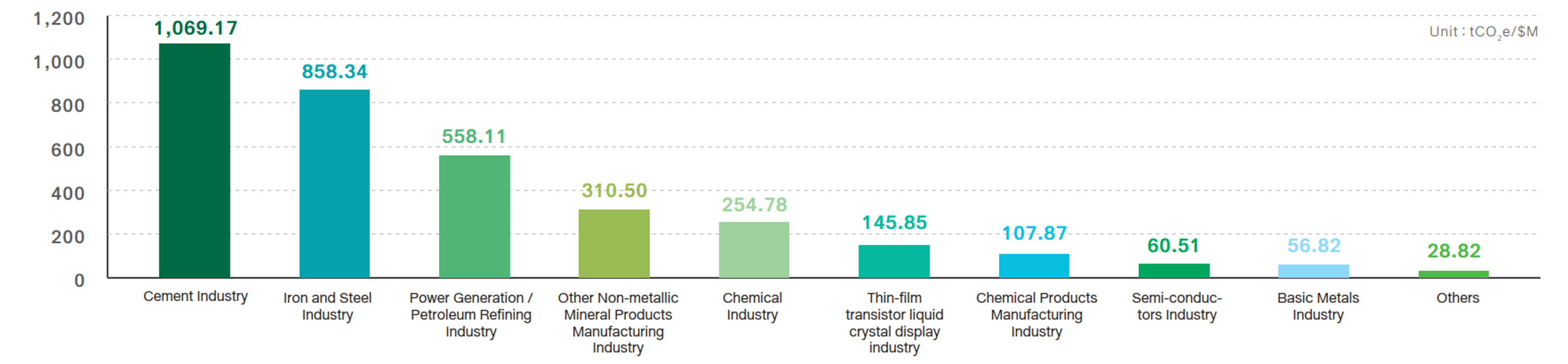

In 2024, the carbon emissions from investment and financing portfolio by industry showed that the top three absolute carbon emitters were "Power Generation / Petroleum Refining Industry (31.21%)", " Iron and Steel Industry (13.69%)", and "Cement Industry (8.52%)". Further analysis of the carbon footprint of the investment and financing portfolio revealed that the highest carbon footprint was from the " Cement Industry ", followed by the " Iron and Steel Industry ", and thirdly the " Power Generation /Petroleum Refining Industry ", with 1,069.17 , 858.34, and 558.11 tCO2e per million USD, respectively.

GHG Emissions of Investment and Financing Portfolio(tCO2e)

Note1:The financed emissions data, categorized by industry, includes only equity investments, corporate bonds, and corporate loans.

Note2:The ranking of absolute greenhouse gas emissions in this section does not include the total emissions from other industries.

Investment and Financing portfolio Carbon Footprint(tCO2e/ USD million)

Regional Comparison

Avoided Emissions

In accordance with the PCAF definition, the SCSB includes project financing for renewable energy projects, such as wind and solar power generation projects, with clearly defined use of purposes, in the project finance category. furthermore, the SCSB calculate the annual avoided emissions of these projects based on the year-end outstanding balance. The following are the project financing data for power plants over the past three years. Moving forward, the SCSB will continue to expand financing for renewable energy power plants to contribute to carbon reduction in the power generation industry.

Green Operations Strategies

Electronic documents and Paperless Policy

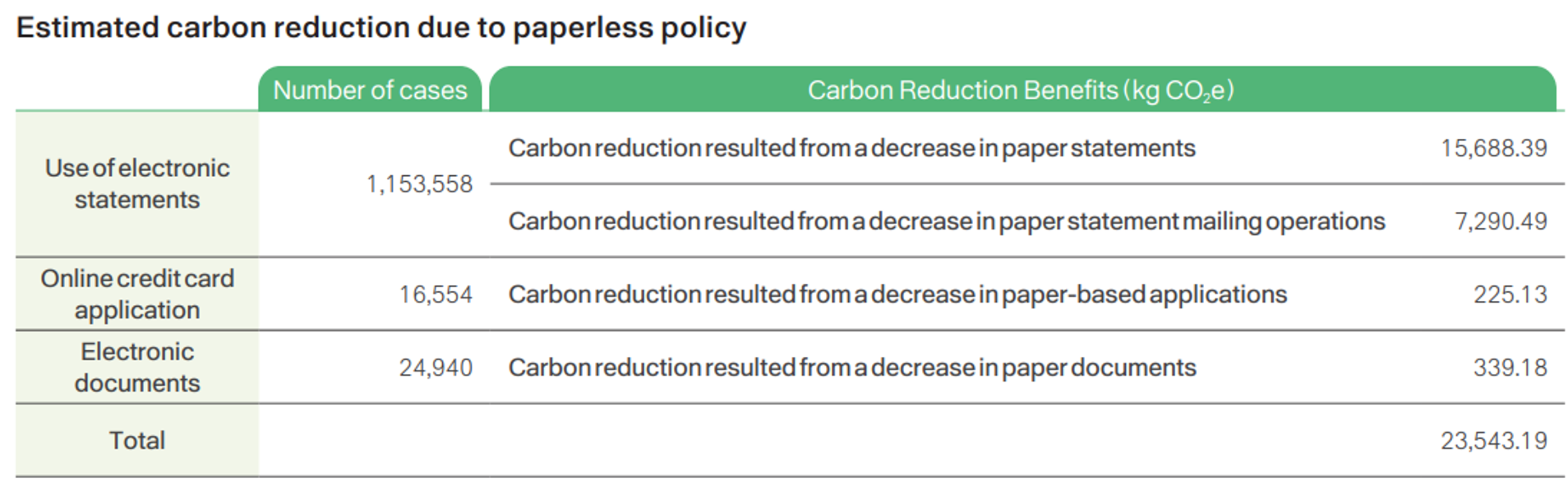

The SCSB continues to encourage customers to apply for credit cards online. Customers who apply for the Minions card online can enjoy a three-year waiver of the annual fee, thereby saving paper and achieving the goal of reducing carbon emissions. In 2024, more than 72.4% of credit card applications were made online, totaling 16,554 applications. If each application uses two A4 sheets of paper, the online credit card application service saved 33,108 sheets of paper.

The SCSB is also promoting the use of electronic statements instead of printed statements. In 2024, the number of customers using only electronic statements reached 157,890, with a total of 1,153,558 electronic statements issued throughout the year. Assuming that each statement and envelope uses two A4 sheets of paper, these customers would collectively save at least 2,307,116 sheets of paper in 2024.

Additionally, the SCSB issued 24,940 electronic documents in 2024. Assuming each document would have used two A4 sheets of paper, this also reduced carbon emissions by approximately 339 kg of CO2e.

According to the Ministry of Environment's Carbon Footprint Information Platform, one A4 sheet of paper has a carbon footprint of 0.0068 kg. In addition, based on the estimation method recommended by the Intergovernmental Panel on Climate Change (IPCC), the mailing process for each physical statement generates approximately 0.0063kg of CO2e. Therefore, the reduction in paper, envelopes, and statement mailing operations due to the SCSB´s paperless efforts in 2024 resulted in a reduction of 23,543 kg of CO2e.

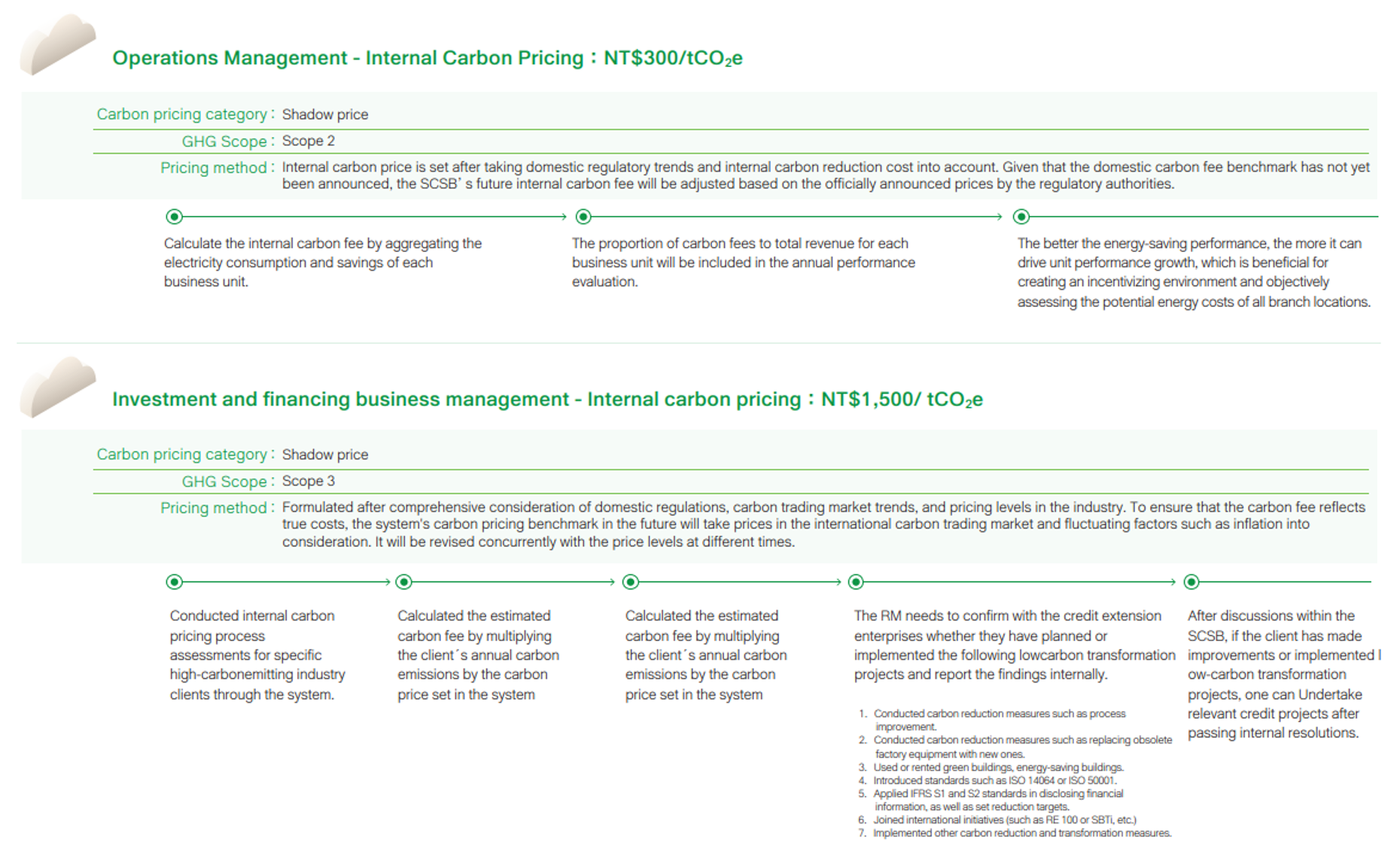

Internal Carbon Pricing and Credit Customer Carbon Fee Risk Assessment

In order to reduce the organization's carbon emissions, the SCSB has begun planning an internal carbon pricing mechnism and developing a carbon fee risk assessment system. By introducing carbon pricing, the SCSB aim to reflect potential carbon costs in our investment and financing decarbonization strategies, as well as in the energy-saving measures at various branch locations. This will encourage employees to implement sustainable environmental actions and serve as a mechanism for managing investment and financing risks.

Column: "Solid Finance, Sustainable Brilliance" – The SCSB’s New Head Office Showcases an Innovative Green Building that Combines Aesthetics with Energy Efficiency

Paris-Aligned Lobbying and Trade Associations

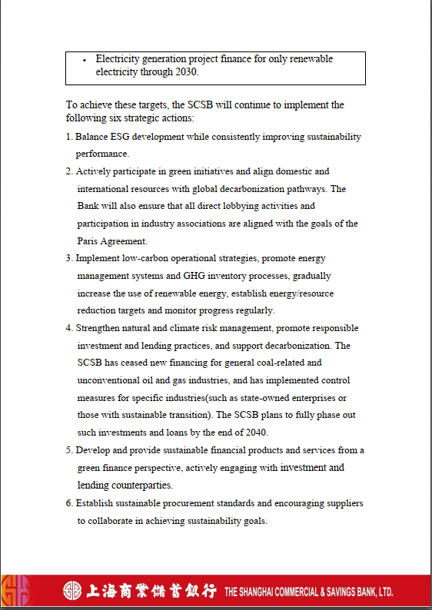

In alignment with our commitment to corporate sustainable development, responding to the international trend towards net-zero emissions, and achieving net-zero emissions by 2050, the SCSB has issued the "The Shanghai Commercial & Savings Bank, Ltd. Declaration on Climate" and established the"Sustainable Development Practices Code" and the "Sustainable Development Promotion Guidelines." These include climate-related management policies and specific implementation plans, serving as the foundation and guiding direction for sustainable development. Additionally, in September 2023, the SCSB announced the "SCSB Sustainable Development Consensus Procedures“, which are aligned with the Paris Agreement. This aims to leverage our financial influence to promote the sustainable development of Environmental, Social, and Governance (ESG) with strategic partners.

To ensure that the SCSB’s direct lobbying activities or participation in trade associations are aligned with the goals of the Paris Agreement, we have established the following management mechanisms to regulate all operational areas of the bank (including overseas branches) and its subsidiaries:

Direct Lobbying Activities

If there is a need for direct lobbying activities, the SCSB will follow the relevant lobbying regulations in each region and adhere to the following management and supervision procedures:

Identify whether the direct lobbying activities are related to climate issues.

Before engaging in direct lobbying activities related to climate policies, ensure that the lobbying content aligns with the Paris Agreement and the bank’s sustainable development policies. The content must be evaluated by the General Management Office and approved by the Sustainable Development Committee (chaired by the General Manager) before proceeding.

The General Management Office will oversee the integration of commercial association participation or lobbying activities, assign specific departments to form task forces based on lobbying topics, and define relevant tasks and responsibilities. The General Management Office will track the execution progress and regularly report the lobbying activity progress and outcomes to the Sustainable Development Committee.

The Sustainable Development Committee will regularly report the progress and results of direct lobbying activities to the Board of Directors.

Trade Associations

For trade associations in which the SCSB participates or intends to participate, the following management and supervision procedures have been established:

Each responsible unit will regularly identify whether the trade associations in which the bank participates or intends to participate are related to climate issues.

Each responsible unit will regularly assess whether the goals of the climate-related trade associations align with the Paris Agreement.

After evaluation, if the goals of the trade associations in which we participate or intend to participate are inconsistent with the bank’s climate change policies and the Paris Agreement, appropriate control measures will be taken, including but not limited to the following actions:

For associations with partially inconsistent climate policy positions, the SCSB will engage in a review and monitoring process as per the Sustainable Development Consensus Procedures, aiming to align the association’s goals with those of the bank within two years. If after this period, the association's climate policies and goals remain inconsistent with those of the bank or the Paris Agreement and no improvements are observed, the SCSB will consider withdrawing financial support or terminating membership.

For associations with c4046ompletely inconsistent climate policy positions, the SCSB will consider directly withdrawing financial support or terminating membership.

If there are any of the above circumstances, the responsible units must report the review and monitoring progress and results to the Sustainable Development Committee.

The Sustainable Development Committee will regularly report the aforementioned review and monitoring progress and results to the Board of Directors.

2024 Assessment Results:

In 2024, the SCSB did not engage in any direct lobbying activities.

In 2024, the trade associations related to climate issues in which the SCSB participated had goals that were consistent with those of the bank and the Paris Agreement. The SCSB completed its SBTi commitment in 2024 and is a founding member of the CommonWealth Magazine Sustainability Association, continually engaging in climate and sustainability exchanges, sharing, and collaborative learning activities across industries. The SCSB is also a member of the Taipei Securities Association, the R.O.C. Bills Finance Association, and The Bankers Association of the Republic of China, jointly advancing sustainable action plans for the financial industry with trade associations.

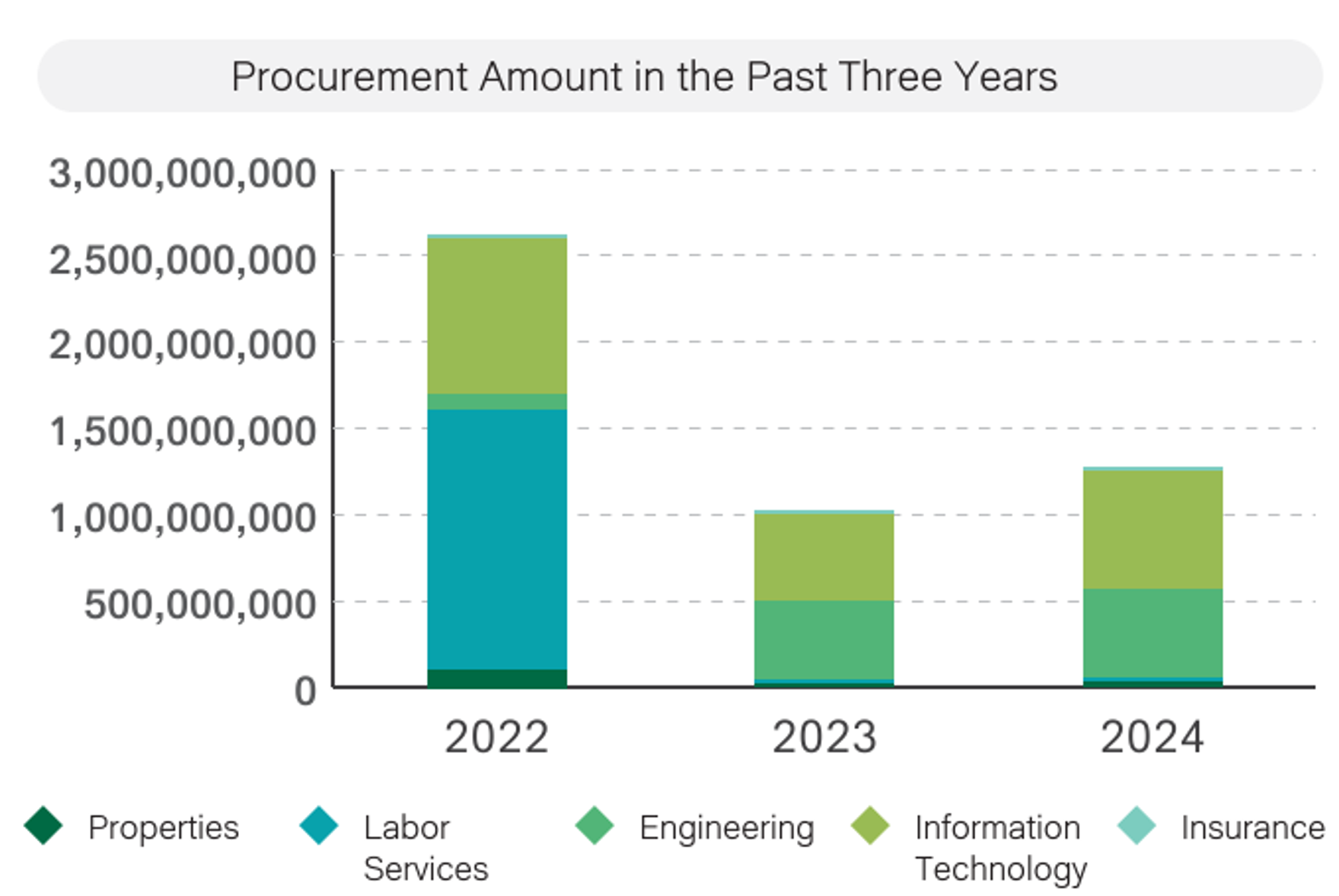

Sustainable Purchase and Supplier Management